US inflation data on Wednesday is the week's centrepiece, but with oil nearing seven-month highs, Bitcoin (BTC) sentiment shifting, and the Australian dollar at three-year highs, traders have plenty to navigate in the week ahead.

Quick Facts

- US inflation rate (February) is the key binary event for rate cut pricing and equity direction.

- Brent crude is trading around US$82–84/bbl, near seven-month highs, with a $4–$10 geopolitical risk premium baked in from Iran/Hormuz tensions.

- Bitcoin is trading above US$70,000 as of 6 March, a potential trend change if it holds through the week.

United States: inflation in focus

Last month’s US inflation reading showed prices rising 2.4% year-on-year, still well above the Fed's 2% target.

February's inflation rate, due Wednesday, will be scrutinised for signs that tariff pass-through or rising energy costs are pushing prices back up, or whether the slow grind lower is still intact.

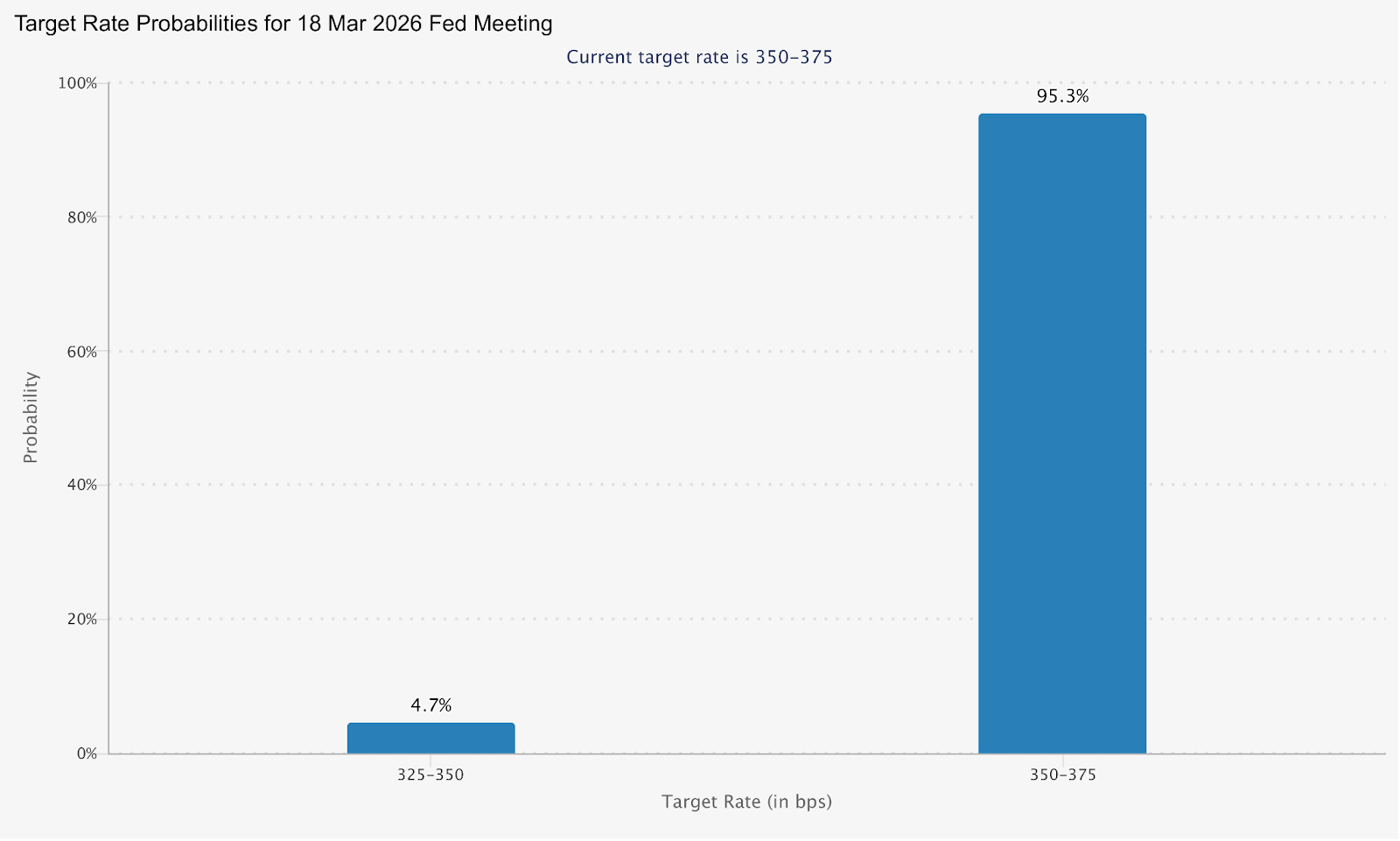

The March FOMC meeting on 17–18 March is now priced at only an 4.7% probability of a cut. A higher-than-expected inflation print this week could potentially push rate cut expectations further out.

A softer read opens the door to renewed cut pricing and potential relief across risk assets.

Key Dates

- US Inflation Rate (February CPI): Wednesday 11 March, 12:30 am (AEDT)

Monitor

- Core vs. headline inflation divergence as evidence of tariff pass-through in goods prices.

- 2-year and 10-year treasury yield sensitivity to the print.

- USD direction and FedWatch repricing in the lead up to the 18 March FOMC decision.

Oil: elevated and event-sensitive

Brent is currently trading around US$83–85 per barrel, with a 52-week range spanning $58.40 to $85.12, reflecting the dramatic move triggered by the Middle East conflict.

Analysts estimate the geopolitical risk premium already baked into oil at US$4–$10 per barrel, and average 2026 Brent forecasts have been lifted to US$63.85/bbl, up from US$62.02 in January.

The EIA's Short-Term Energy Outlook forecasts Brent to average $58/bbl in 2026, well below the current spot price.

The gap between spot and the forecast baseline could be a useful frame for traders this week: any de-escalation signal from the Middle East could rapidly close that gap.

Monitor

- Strait of Hormuz developments and any diplomatic signals from Iran nuclear talks.

- EIA weekly oil inventory data.

- Oil's knock-on to inflation expectations and whether it shifts central bank posture.

- Energy sector equity performance relative to the broader market.

Bitcoin: sentiment watch

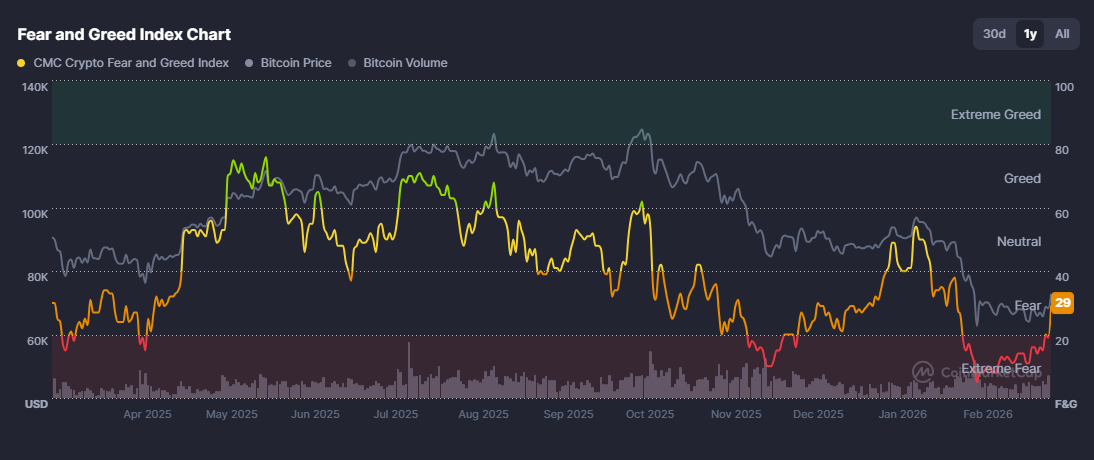

BTC has been attempting to stabilise after a brutal 53% correction over the past 17 weeks, fuelled by escalating geopolitical tensions and renewed tariff concerns.

However, yesterday saw a 8% jump back above $72,000, and the crypto “fear and greed index” jumped up to 29 (fear), up from below 20 (extreme fear), where it has been sitting for over a month, indicating a potential sentiment shift.

A cooler-than-expected US inflation print on Wednesday could provide further fuel for the breakout; a hot print risks potentially pulling BTC back below the US$70,000 level it has just reclaimed.

Monitor

- Inflation print reaction on Wednesday as the primary macro catalyst for the move.

- Any rotation into altcoins following BTC strength.

- ETF inflow/outflow data as confirmation of institutional participation.

AUD/USD: Hawkish RBA meets geopolitical crosswinds

The Aussie is trading near more than three-year highs and heading for its fourth consecutive monthly gain, up more than 6% year-to-date, making it the top-performing G10 currency in 2026.

The driver is a clear policy divergence. RBA Governor Michele Bullock signalled the March policy meeting is "live" for a possible rate increase, and warned that an oil price shock from Iran tensions could reignite domestic inflationary pressures.

Market pricing now suggests around a 28% chance of a 25bp hike at the upcoming meeting, while fully pricing in tightening through May, and around a 75% chance of another increase to 4.35% by year-end.

This hawkish read, set against a Fed on hold and facing dovish political pressure, creates a potential structural tailwind for the Aussie.

Monitor

- AUD/USD reaction to Wednesday's US inflation data.

- RBA rate hike probability repricing through the week.

- Iron ore and commodity prices as secondary AUD drivers.

- China demand signals, given Australia's export exposure.

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.