Market news & insights

Stay ahead of the markets with expert insights, news, and technical analysis to guide your trading decisions.

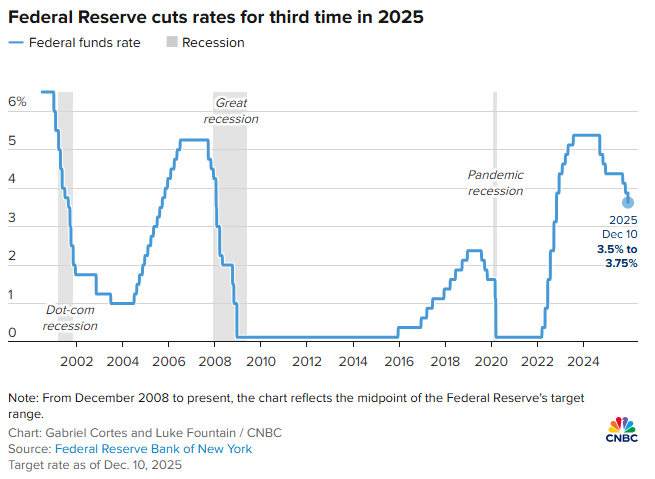

The Federal Reserve delivered its third consecutive rate cut this morning, lowering rates 25 basis points to 3.5%-3.75% after a 9-3 vote in favour.

The three dissents were the most seen since September 2019. Governor Stephen Miran pushed for a steeper 50bp cut while regional presidents Jeff Schmid and Austan Goolsbee wanted to hold steady.

Four additional non-voting participants also preferred no cut at all, exposing deep disalignment on the best policy path going forward.

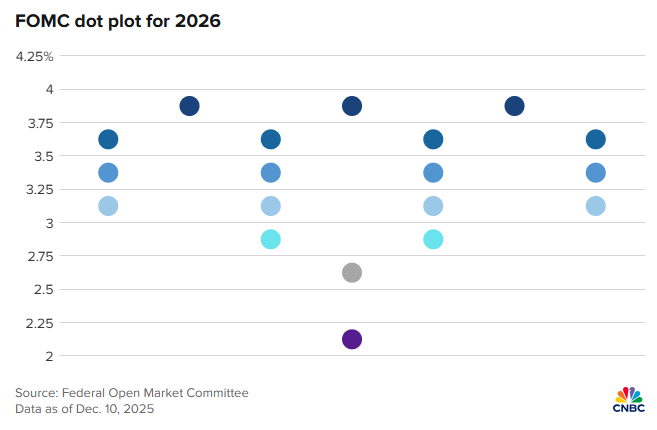

The updated Federal Reserve dot plot maintained projections for just one cut in 2026 and another in 2027, unchanged from September despite three cuts delivered since then.

Seven officials now see no cuts needed next year, while three believe rates are already too low, suggesting the divide between members is set to continue growing in 2026.

In his post-meeting press conference, Fed chair Jerome Powell explicitly stated, "We are well positioned to wait and see how the economy evolves." — phrasing last used when the Fed paused cuts for nine months.

However, with Powell's tenure ending in January and Trump publicly demanding deeper cuts, the Fed continues to face mounting pressure, further clouding 2026 projections.

Markets are currently pricing Kevin Hassett as the next chair, thanks to his apparent accommodation to Trump’s preferences.

Oracle Stock Plummets as Revenue Falls Short of Estimates

Oracle Corporation suffered a 10%+ after-hours selloff today, following fiscal second-quarter results that exposed mounting risks beneath its ambitious AI infrastructure buildout.

Revenue of $16.06 billion fell short of the $16.21 billion Wall Street consensus, triggering a sharp reassessment of one of the most leveraged bets in the AI sector.

The company's total debt now exceeds $105 billion, and the cost of insuring Oracle's debt against default reached its highest level since March 2009, rising to about 1.28 percentage points per year.

Further investor anxiety lies in Oracle's dependence on its contract with OpenAI, which is estimated to account for about 58% of Oracle's future order backlog.

The contract requires OpenAI to pay approximately $60 billion annually to Oracle starting in 2027. However, OpenAI currently only generates around $20 billion in annualised revenue, exposing Oracle to massive counterparty risk if OpenAI doesn’t meet its revenue projections.

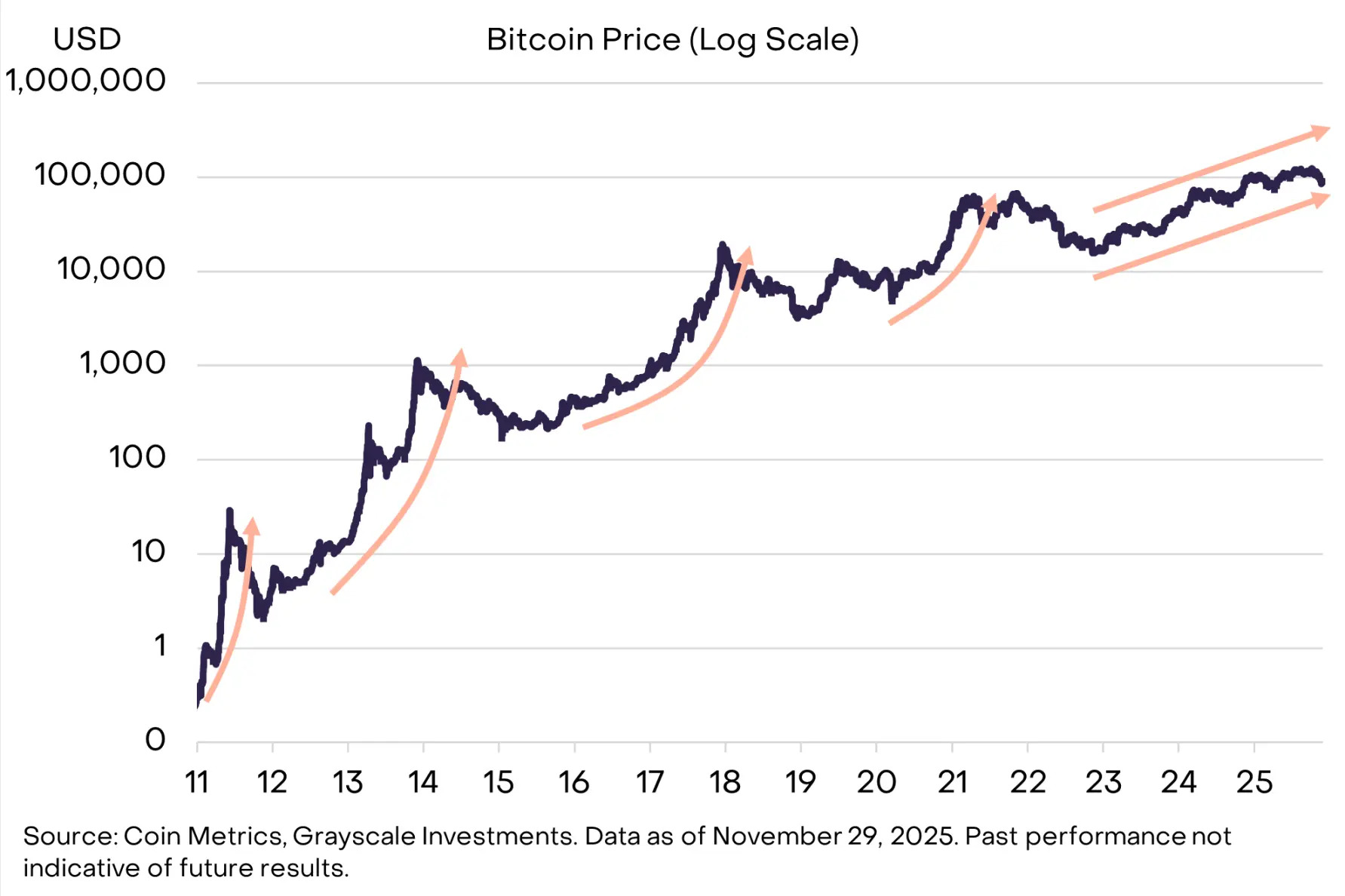

Bitcoin Price Narratives Get Murkier

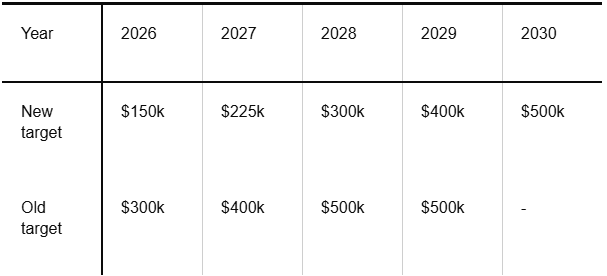

Standard Chartered slashed its 2026 Bitcoin price target from $300,000 to $150,000 yesterday.

Attributed to the apparent end of aggressive corporate Bitcoin accumulation and slower-than-expected institutional adoption through ETFs, it is one of the most dramatic forecast reductions this year.

The bank's updated forecasts project $100,000 by end-2025, $150,000 for end-2026, $225,000 for end-2027, $300,000 for end-2028, and $400,000 for end-2029.

Despite the revision, Standard Chartered explicitly rejects the notion that we have entered a new crypto winter, characterising the current phase as "a cold breeze" rather than structural weakness.

Broader market predictions for 2026 suggest a bearish scenario at $95,241, an average estimate of $111,187, and a bullish case of $142,049.

InvestingHaven forecasts Bitcoin trading between a minimum of $99,910 and a maximum of $200,000 in 2026.

And some bullish analysts like Cardano founder Charles Hoskinson have suggested Bitcoin could reach $250,000 in 2026 if tech giants increase their crypto exposure, indicating considerable divergence in expectations.

.jpg)

US markets are eyeing all-time highs following strong data and earnings reports. Whether these records are achieved will depend on the news flow over the coming days, particularly from the Federal Reserve.

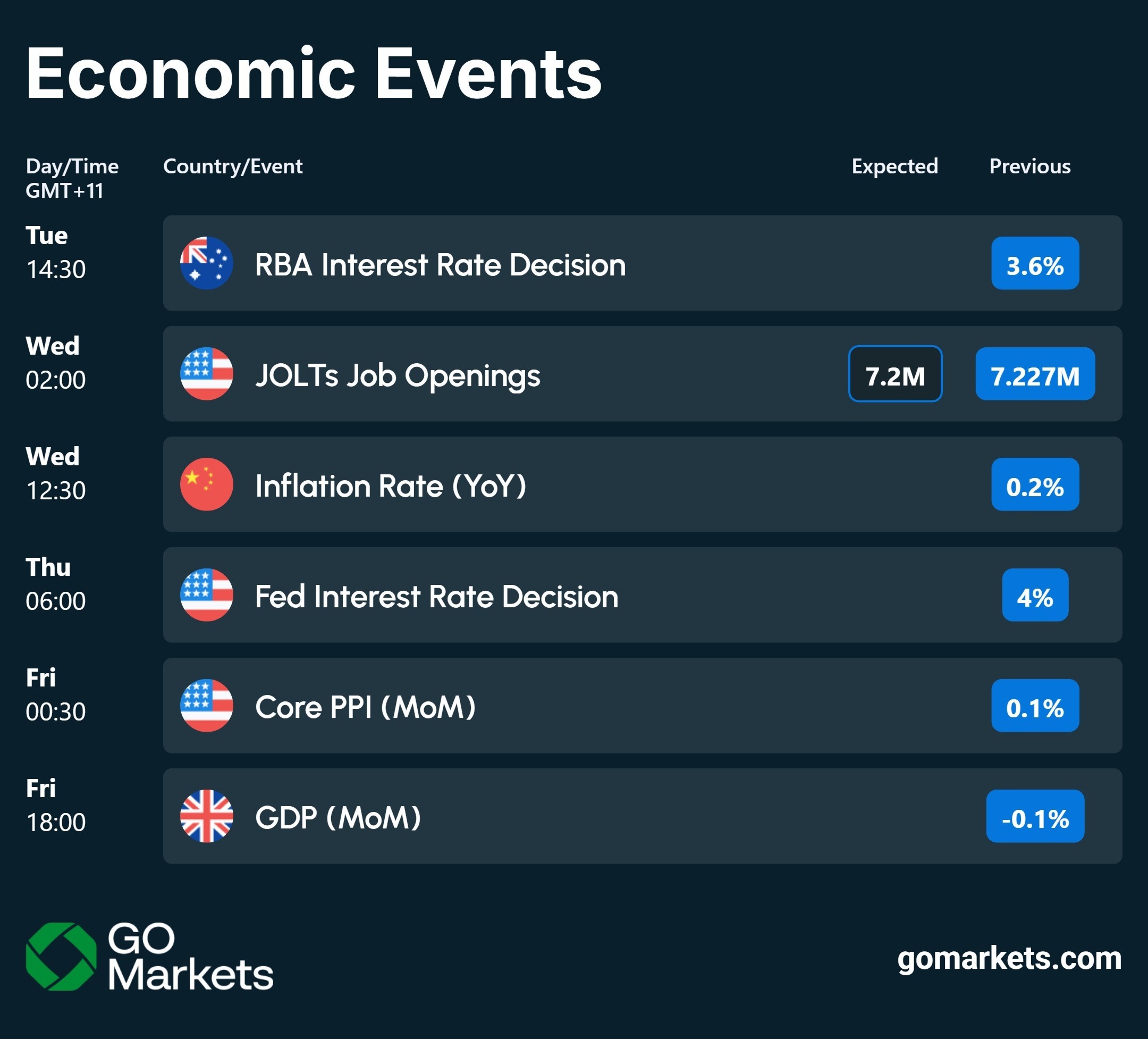

Fed Decision Incoming

The Federal Reserve's two-day meeting will end this Wednesday with a 0.25% rate cut widely expected. But following Friday's encouraging PCE numbers, the bigger question is “Will there be a January cut?” The Fed press conference post-decision will likely the highest signal event for the rest of 2025.

Central Bank Decisions Everywhere

Beyond the Fed, the Reserve Bank of Australia meets tomorrow with a pause expected, as recent data hasn't provided sufficient incentive for another cut. The ECB, Bank of England, and Bank of Japan will also all announce decisions within the next ten days, creating potential volatility across both equity and FX markets.

Big Tech Earnings

Two major AI infrastructure players report earnings this week: Broadcom and Oracle. These reports come at a time when AI valuations are under heavy public scrutiny, however, they will likely take a backseat to whatever the Fed signals about its 2026 path.

Copper Breaks Out

Copper has rallied to a four-month high and is now testing the $5.50 level. After breaching the key $5.25 support level, the market is showing some hesitation in Asia ahead of major data releases and the Fed decision. The July record highs of $5.50 are now within reach, though it is still to be seen if this level holds or if we pull back toward $5.25 support.

Market Insights

Watch Mike Smith's analysis of the week ahead in markets.

Key Economic Events

Stay up to date with the key economic events for the week.

.jpg)

Bitcoin rebounded 7% to touch $94,000 this week as two of the world's largest asset managers doubled down on their conviction that this cycle could break from crypto's boom-bust past.

BlackRock CEO Larry Fink and COO Rob Goldstein declared tokenisation "the next major evolution in market infrastructure,” comparing its potential to the introduction of electronic messaging systems in the 1970s.

Tokenised real-world assets have exploded from $7 billion to $24 billion in just one year, with certain projections expecting tokenised instruments to comprise 10-24% of portfolios by 2030.

Grayscale's latest research also put forward the case that this cycle will not follow Bitcoin’s predictable four-year pattern. Their analysis shows this cycle has had no parabolic price surge like previous cycles, and capital is flowing through regulated ETPs and corporate treasuries rather than retail speculation.

Grayscale has boldly predicted Bitcoin will reach new all-time highs next year based on this data, with near-term catalysts including a likely Federal Reserve rate cut and advancing crypto legislation.

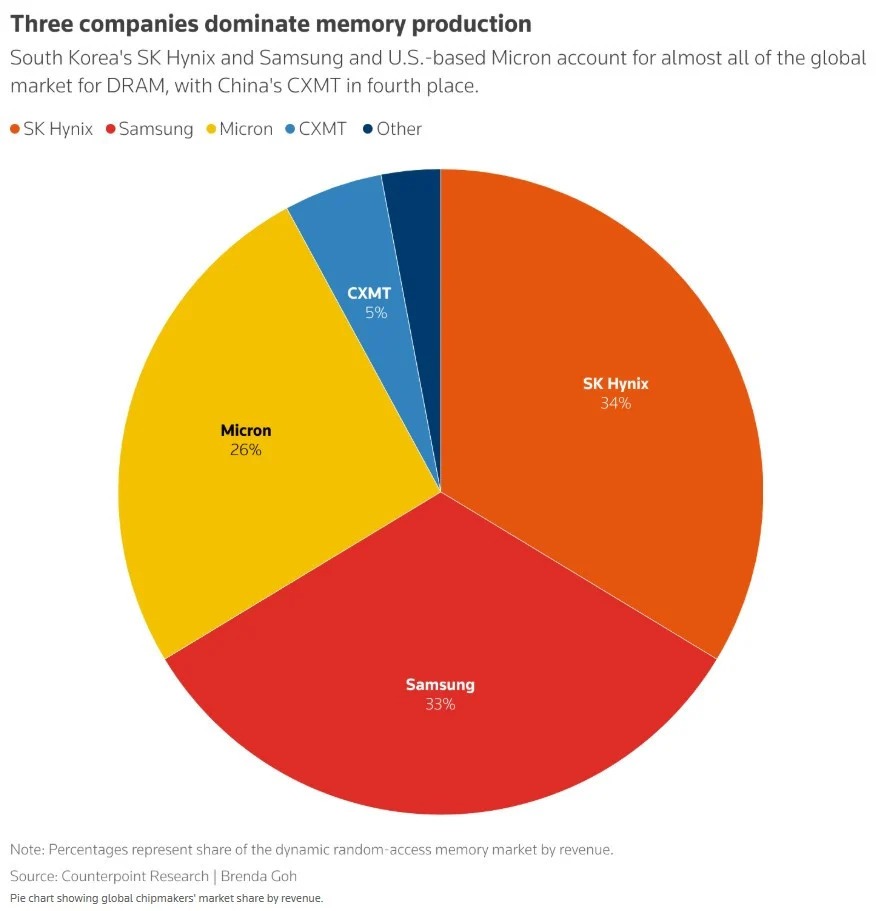

AI Boom Creating a Memory Chip Supply Crisis

The AI revolution has had an unexpected ripple effect on conventional memory chips (DRAM).

Post-ChatGPT launch in 2022, chipmakers pivoted aggressively toward high-bandwidth memory (HBM) chips — the components that power AI data centres.

Samsung and SK Hynix, who control roughly 70% of the global DRAM market, transitioned large portions of their production away from conventional chips.

This worked in the short term, but data centre operators are now replacing old servers, and PC and smartphone sales have exceeded expectations (all of which require DRAM).

This saw DRAM supplier inventories fall to just two to four weeks in October, down from 13 to 17 weeks in late 2024.

DRAM spot prices nearly tripled in September this year, while in Tokyo's electronics district, popular gaming memory modules have surged from 17,000 yen to over 47,000 yen in recent weeks.

Google, Amazon, Microsoft, and Meta have all approached Micron with open-ended orders, agreeing to purchase whatever the company can deliver, regardless of price.

Samsung, Micron, and SK Hynix shares have rallied 96%, 168%, and 213% YTD, respectively, thanks to the increased DRAM demand.

Ironically, this recent price surge has seen DRAM chip margins approach those of the advanced HBM chips, meaning non-AI memory could now become equally profitable to produce.

Buying Pressure Pushes Copper Through Key Level

.jpg)

Every trader has had that moment where a seemingly perfect trade goes astray.

You see a clean chart on the screen, showing a textbook candle pattern; it seems as though the market planets have aligned, and so you enthusiastically jump into your trade.

But before you even have time to indulge in a little self-praise at a job well done, the market does the opposite of what you expected, and your stop loss is triggered.

This common scenario, which we have all unfortunately experienced, raises the question: What separates these “almost” trades from the truly higher-probability setups?

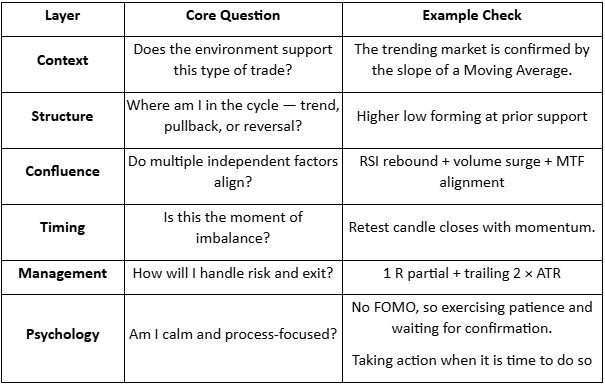

The State of Alignment

A high-probability setup isn’t necessarily a single signal or chart pattern. It is the coming together of several factors in a way that can potentially increase the likelihood of a successful trade.

When combined, six interconnected layers can come together to form the full “anatomy” of a higher-probability trading setup:

- Context

- Structure

- Confluence

- Timing

- Management

- Psychology

When more of these factors are in place, the greater the (potential) probability your trade will behave as expected.

Market Context

When we explore market context, we are looking at the underlying background conditions that may help some trading ideas thrive, and contribute to others failing.

Regime Awareness

Every trading strategy you choose to create has a natural set of market circumstances that could be an optimum trading environment for that particular trading approach.

For example:

- Trending regimes may favour momentum or breakout setups.

- Ranging regimes may suit mean-reversion or bounce systems.

- High-volatility regimes create opportunity but demand wider stops and quicker management.

Investing time considering the underlying market regime may help avoid the temptation to force a trending system into a sideways market.

Simply looking at the slope of a 50-period moving average or the width of a Bollinger Band can suggest what type of market is currently in play.

Sentiment Alignment

If risk sentiment shifts towards a specific (or a group) of related assets, the technical picture is more likely to change to match that.

For example, if the USD index is broadly strengthening as an underlying move, then looking for long trades in EURUSD setups may end up fighting headwinds.

Setting yourself some simple rules can help, as trading against a potential tidal wave of opposite price change in a related asset is not usually a strong foundation on which to base a trading decision.

Key Reference Zones

Context also means the location of the current price relative to levels or previous landmarks.

Some examples include:

- Weekly highs/lows

- Prior session ranges, e.g. the Asian high and low as we move into the European session

- Major “round” psychological numbers (e.g., 1.10, 1000)

A long trading setup into these areas of market importance may result in an overhead resistance, or a short trade into a potential area of support may reduce the probability of a continuation of that price move before the trade even starts.

Market Structure

Structure is the visual rhythm of price that you may see on the chart. It involves the sequences of trader impulses and corrections that end up defining the overall direction and the likelihood of continuation:

- Uptrend: Higher highs (HH) and higher lows (HL)

- Downtrend: Lower highs (LH) and lower lows (LL)

- Transition: Break in structure often followed by a retest of previous levels.

A pullback in an uptrend followed by renewed buying pressure over a previous price swing high point may well constitute a higher-probability buy than a random candle pattern in the middle of nowhere.

Compression and Expansion

Markets move through cycles of energy build-up and release. It is a reflection of the repositioning of asset holdings, subtle institutional accumulation, or a response to new information, and may all result in different, albeit temporary, broad price scenarios.

- Compression: Evidenced by a tightening range, declining ATR, smaller candles, and so suggesting a period of indecision or exhaustion of a previous price move,

- Expansion: Evidenced by a sudden breakout, larger candle bodies, and a volume spike, is suggestive of a move that is now underway.

A breakout that clears a liquidity zone often runs further, as ‘trapped’ traders may further fuel the move as they scramble to reposition.

A setup aligned with such liquidity flows may carry a higher probability than one trading directly into it.

Confluence

Confluence is the art of layering independent evidence to create a whole story. Think of it as a type of “market forensics” — each piece of confirmation evidence may offer a “better hand’ or further positive alignment for your idea.

There are three noteworthy types of confluence:

- Technical Confluence – Multiple technical tools agree with your trading idea:

- Moving average alignment (e.g., 20 EMA above 50 EMA) for a long trade

- A Fibonacci retracement level is lining up with a previously identified support level.

- Momentum is increasing on indicators such as the MACD.

- Multi-Timeframe Confluence – Where a lower timeframe setup is consistent with a higher timeframe trend. If you have alignment of breakout evidence across multiple timeframes, any move will often be strengthened by different traders trading on different timeframes, all jumping into new trades together.

3. Volume Confluence – Any directional move, if supported by increasing volume, suggests higher levels of market participation. Whereas falling volume may be indicative of a lesser market enthusiasm for a particular price move.

Confluence is not about clutter on your chart. Adding indicators, e.g., three oscillators showing the same thing, may make your chart look like a work of art, but it offers little to your trading decision-making and may dilute action clarity.

Think of it this way: Confluence comes from having different dimensions of evidence and seeing them align. Price, time, momentum, and participation (which is evidenced by volume) can all contribute.

Timing & Execution

An alignment in context and structure can still fail to produce a desired outcome if your timing is not as it should be. Execution is where higher probability traders may separate themselves from hopeful ones.

Entry Timing

- Confirmation: Wait for the candle to close beyond the structure or level. Avoid the temptation to try to jump in early on a premature breakout wick before the candle is mature.

- Retests: If the price has retested and respected a breakout level, it may filter out some false breaks that we will often see.

- Then act: Be patient for the setup to complete. Talking yourself out of a trade for the sake of just one more candle” confirmation may, over time, erode potential as you are repeatedly late into trades.

Session & Liquidity Windows

Markets breathe differently throughout the day as one session rolls into another. Each session's characteristics may suit different strategies.

For example:

- London Open: Often has a volatility surge; Range breaks may work well.

- New York Overlap: Often, we will see some continuation or reversal of morning trends.

- Asian Session: A quieter session where mean-reversion or range trading approaches may do well

Trade Management

Managing the position well after entry can turn probability into realised profit, or if mismanaged, can result in losses compounding or giving back unrealised profit to the market.

Pre-defined Invalidation

Asking yourself before entry: “What would the market have to do to prove me wrong?” could be an approach worth trying.

This facilitates stops to be placed logically rather than emotionally. If a trade idea moves against your original thinking, based on a change to a state of unalignment, then considering exit would seem logical.

Scaling & Partial Exits

High-probability trade entries will still benefit from dynamic exit approaches that may involve partial position closes and adaptive trailing of your initial stop.

Trader Psychology

One of the most important and overlooked components of a higher-probability setup is you.

It is you who makes the choices to adopt these practices, and you who must battle the common trading “demons” of fear, impatience, and distorted expectation.

Let's be real, higher-probability trades are less common than many may lead you to believe.

Many traders destroy their potential to develop any trading edge by taking frequent low-probability setups out of a desire to be “in the market.”

It can take strength to be inactive for periods of time and exercise that patience for every box to be ticked in your plan before acting.

Measure “You” performance

Each trade you take becomes data and can provide invaluable feedback. You can only make a judgment of a planned strategy if you have followed it to the letter.

Discipline in execution can be your greatest ally or enemy in determining whether you ultimately achieve positive trading outcomes.

Bringing It All Together – The Setup Blueprint

Final Thoughts

Higher-probability setups are not found but are constructed methodically.

A trader who understands the “higher-probability anatomy” is less likely to chase trades or feel the need to always be in the market. They will see merit in ticking all the right boxes and then taking decisive action when it is time to do so.

It is now up to you to review what you have in place now, identify gaps that may exist, and commit to taking action!

.jpg)

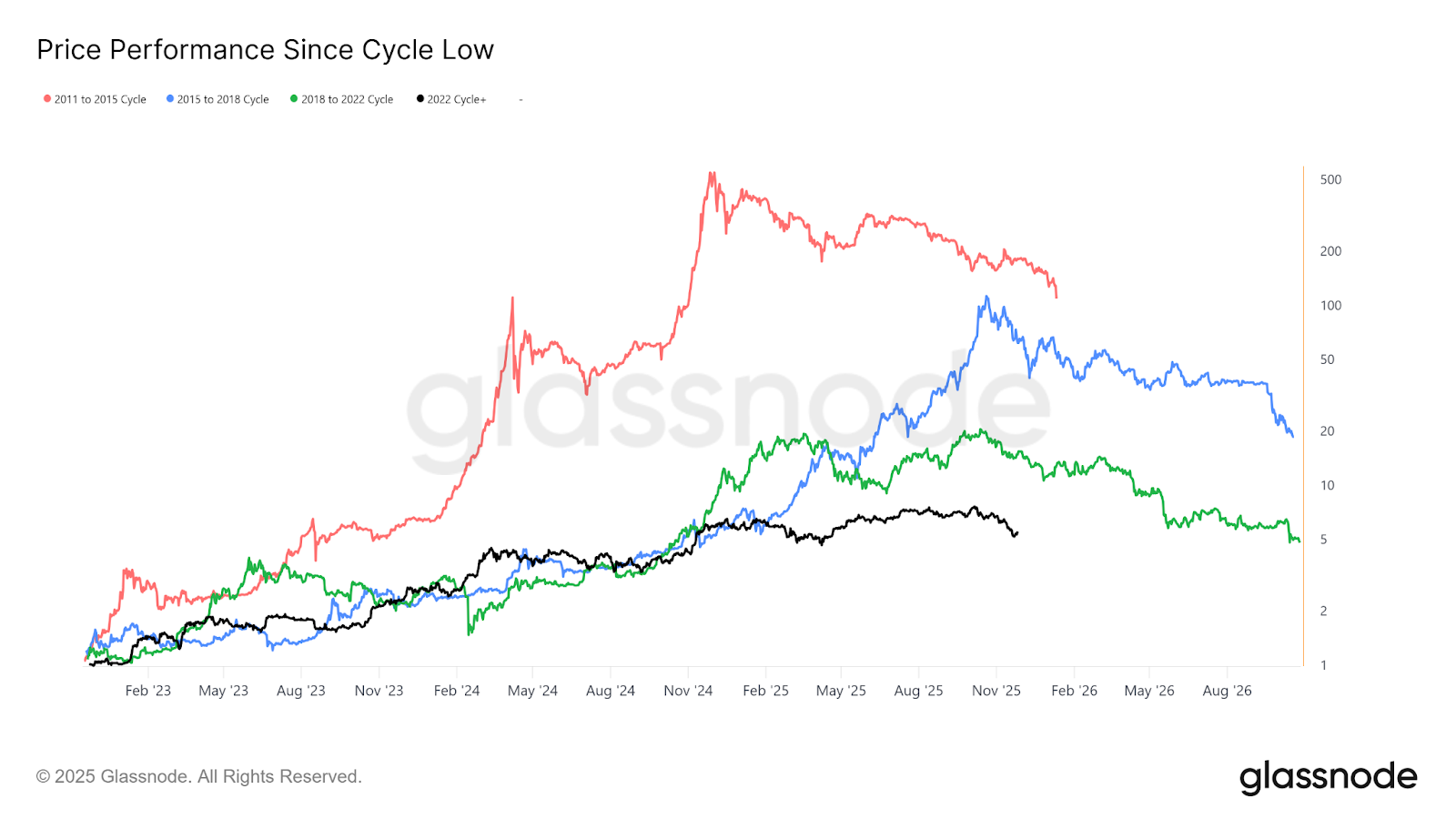

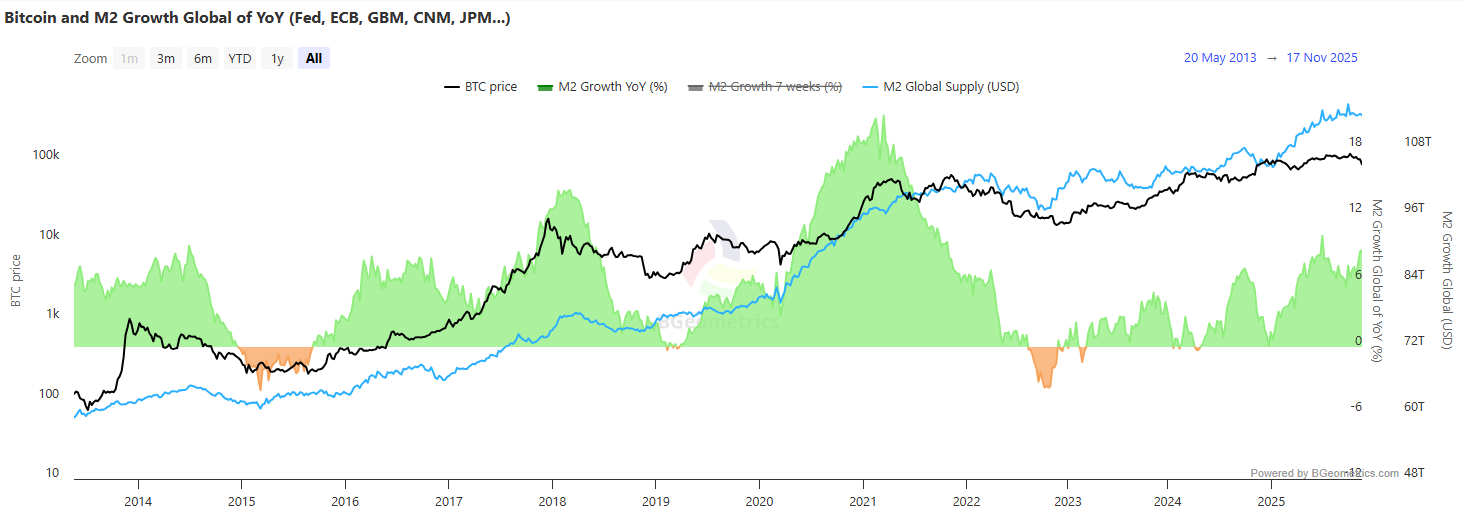

Bitcoin has now outlasted the peak of all its previous four-year cycles.

For over a decade, every Bitcoin cycle has followed the same sequence: consolidation, breakout, mania, crash. Rinse and repeat.

Timeline-wise, we should be at the post-mania inflection point, waiting for the seemingly inevitable crash.

Yet unlike previous runs, this cycle never saw its “mania phase.” Instead, Bitcoin has spent the past year grinding sideways, touching new all-time highs without a euphoric blow-off top that defined previous cycles.

The fact that this euphoria period never materialised brings into question whether this cycle still has room to run, or has the market simply matured past the point of mania-driven peaks?

The Historical Four-Year Pattern

The traditional Bitcoin cycle was simple. Every four years, a halving event would reduce the block reward (amount of new Bitcoin being created) by half, creating a supply shock that triggered major bull markets.

The 2013 cycle, the 2017 cycle, and the 2021 cycle all followed this script. Each halving was followed by a 3-to 9-month growth period, then a full-on mania period, before topping out 12 to 18 months after the event.

Following the most recent halving in April 2024, Bitcoin experienced five months of sideways consolidation, then hinted at making its anticipated breakout into mania after the US election… but quickly returned to sideways consolidation for the next year.

We have seen new ATHs and the price has made some notable gains during the period, but the overall momentum has been much weaker.

This failure to repeat the frenzies of the past three cycles has brought into question how much influence the Bitcoin halving truly has on the market anymore.

No Longer a Supply Shock

In previous cycles, the halving created a situation where prices had to rise to clear the same dollar amount of miner expenses (who were now earning half the Bitcoin).

Bitcoin miners would simply not sell until the price reached a certain level, creating a supply shock that would drive prices higher.

Miners still do this today; however, the market’s maturation and the institutional adoption of Bitcoin have dampened the impact.

Selling off Bitcoin is no longer a balancing act where miners hold influence over price. The market has deep liquidity that can handle significant flows in either direction.

Institutional ETFs routinely purchase more Bitcoin in a single day than miners produce in a month.

The supply reduction that once drove dramatic price movements is now easily absorbed by a market with institutional buyers providing constant demand.

If the Halving Isn't Driving Cycles, What Is?

The overriding narrative is that the Bitcoin cycle is now tied to the global liquidity cycle.

If you plot the Global M2 Money Supply versus Bitcoin on a year-on-year basis, you can see that every Bitcoin top has correlated with the peaks of Global M2 liquidity growth.

This isn't unique to Bitcoin. The Gold price has closely mirrored the rate of Global M2 expansion for decades.

When central banks flood the system with liquidity, capital tends to move into stores of value or high-risk assets. When they drain liquidity, those same assets tend to retreat.

However, this is a correlation; these relationships may change and should not be relied upon as indicators of future performance.

Is the Dollar Just Getting Weaker?

The U.S. Dollar Strength Index tells the other side of this liquidity story. Bitcoin versus the dollar year-on-year has been almost perfectly inversely correlated.

Simply put, as fiat currencies lose purchasing power, “hard” assets like Bitcoin and Gold start to appreciate. Not because of improved fundamentals, but because the currencies they are paired against are simply worth less.

The Self-Fulfilling Prophecy

Beyond the charts and patterns, there is also the psychological notion that the four-year cycle persists precisely because people believe it will.

People have been conditioned by three complete cycles to expect Bitcoin to peak somewhere between 400 and 600 days after a halving.

This collective belief shapes behaviour: traders take profits, investors take fewer risks, and retail enthusiasm wanes. The prophecy fulfils itself.

When everyone believes Bitcoin should peak 18 months after a halving, the combined selling pressure can create exactly that outcome — regardless of whether the underlying driver still exists.

The current market weakness, with Bitcoin dropping over 20% from its October record high, occurred almost precisely at this 18-month mark.

Is This Cycle Built Different?

Despite this on-cue sell-off, this cycle still has the potential to break away from the historical four-year pattern.

Increased ETF adoption by institutional investors has brought in higher quality and consistent ownership of Bitcoin.

Unlike retail traders, who often panic-sell during corrections, institutional holders tend to maintain their positions through volatility.

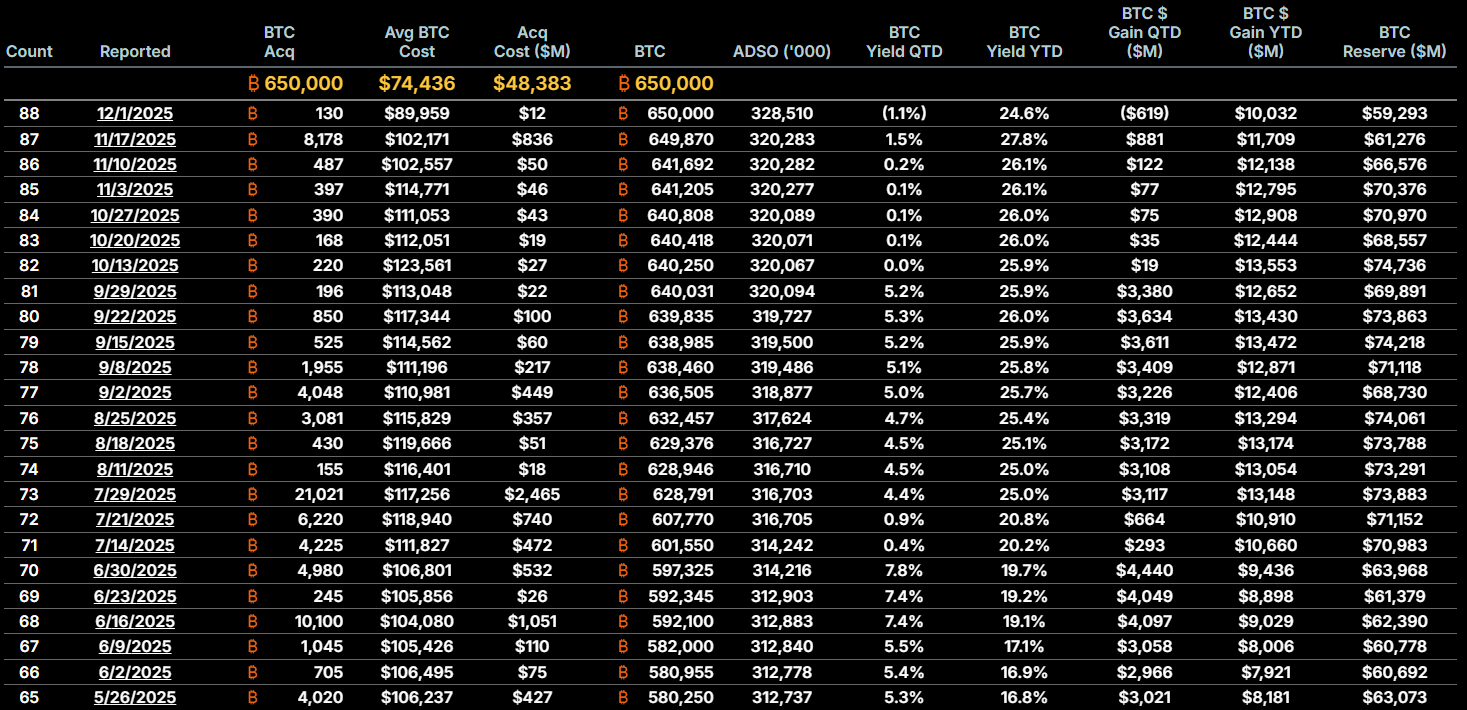

For example, Michael Saylor’s high-profile MicroStrategy fund has continued to purchase Bitcoin through market weakness. Recently reporting a purchase of 8,178 BTC at an average price of $102,171.

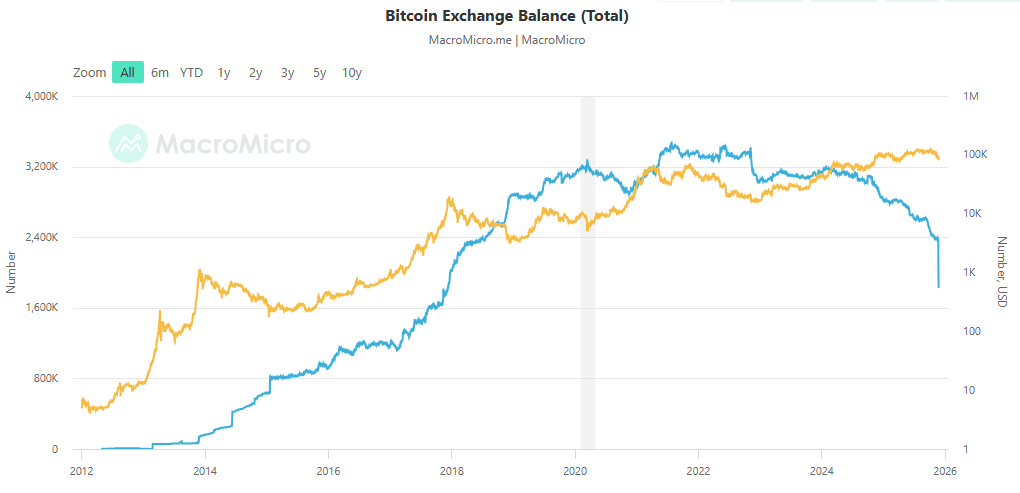

Another hard indicator that diverges from previous cycle peaks is the amount of Bitcoin being held on centralised exchanges.

The current amount of BTC on CEXs is unusually low. This pattern is generally seen closer to cycle lows, rather than peaks.

Other factors supporting the break of the four-year mould are coming out of the Whitehouse.

A comprehensive regulatory framework through the CLARITY Act represents structural changes and boundaries for regulatory bodies that didn't exist in previous cycles.

And the move to establish a Strategic Bitcoin Reserve will see all government-held forfeited Bitcoin (approximately $30 billion worth) transferred into a government reserve, signalling Bitcoin as a strategic asset like Gold and oil.

Bitcoin Has Finally Grown Up

The four-year cycle has been a useful heuristic, but heuristics break down when conditions change. Institutional buyers, regulatory clarity, and strategic reserves represent genuinely new conditions historical patterns don’t account for.

At the same time, dismissing the cycle entirely would be premature. The self-fulfilling aspect means it retains predictive power even if the original cause has weakened.

Market participants act on the pattern they've learned, and their actions create the pattern they expect.

Perhaps the real insight is that the Bitcoin market cycles never had just one cause. They were always the result of multiple overlapping forces — programmed scarcity, liquidity conditions, sentiment, self-reinforcing expectations.

The cycle shifts character as some forces strengthen and others weaken. But whether the forces have shifted enough to break the four-year trend is yet to be determined.

The fundamental indicators show this cycle may have some life, but the psychological power of the four-year pattern could push it to another, predictable end.

You can trade BTC and other popular Crypto CFD pairs on GO Markets with $0 swaps until 31 December 2025.

.jpg)

Markets have bounced back strongly this week. The S&P 500 is now just 1.5% from record highs, and the Nasdaq is recovering well following its pullback.

Rate Cut Expectations

The main driver behind this rally was a shift in Federal Reserve rate cut expectations. Markets are currently pricing in a quarter-point rate cut for December, with only a 25% chance of another reduction in January. This week's economic data will be crucial in shaping expectations going into 2026.

Key Economic Data This Week

Several important data releases are scheduled for this week. The PCE inflation data — the Fed's preferred inflation measure — for September will finally be released on Friday and could have the biggest impact on December and January rate decisions. The ADP jobs report and weekly jobless claims will also be released, while the non-farm payrolls report has been delayed again.

Global Manufacturing Snapshot

Today also kicks off a busy week of manufacturing data releases. Global PMI numbers are due across the board, including figures from the Eurozone, UK, Germany, and the US this evening. These reports will provide a critical snapshot of global economic health and could help reveal the impact of the US trade tariffs.

Gold Breaks Higher

Gold made a significant move on Friday, breaching the key $4,200 level after consolidating last week. The precious metal has followed through today, and the $4,400 level now looks achievable if buying pressure continues.

Bitcoin Under Pressure

Bitcoin has given up last week's modest gains and seen substantial selling pressure. A significant drop of about $4,000 occurred during Asian trading this morning — a notable decline for an Asia session. The key level to watch is $84,000, with potential support at $80,000 (the lowest level since March).

Market Insights

Watch Mike Smith's analysis of the week ahead in markets.

Key Economic Events

Stay up to date with the key economic events for the week.

.jpg)

Nvidia's AI computing dominance is facing its most serious challenge yet, with Google strengthening its position as an equal competitor in the AI chip market this week.

Google’s newest AI model, Gemini 3, was announced to be powered by Google’s in-house tensor processing units (TPUs) a few weks ago. A blow to Nvida, but not a huge shock.

However, this week it was announced that Google is now negotiating with Meta to supply billions of dollars' worth of its TPUs for Meta's data centres in 2027.

Google is reported to be pitching its cloud customers on TPU purchases, claiming it could capture as much as 10% of Nvidia's annual revenue.

Nvidia Shares fell 2.6% following the Google-Meta report and are down 10% for the month, erasing more than $500 billion in market value.

For Google, this represents pure upside—monetising technology development while a competitor helps fund the operation.

Meta also stands to benefit from presumably lower costs compared to Nvidia's premium-priced GPUs.

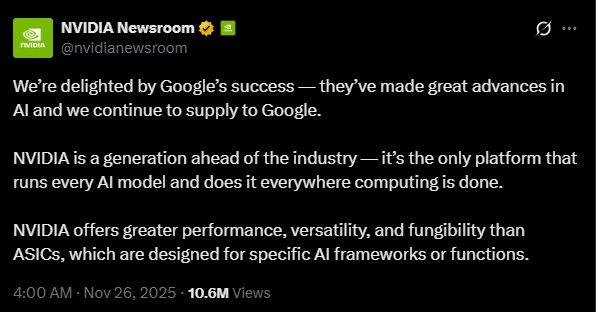

Nvidia maintains it is "a generation ahead of the industry" and emphasises that it offers greater performance, versatility, and fungibility than application-specific integrated circuits (ASICs) like Google's TPUs.

Yet the very act of addressing these concerns—after years of untouchable dominance—may signal the pressure mounting on the AI chip leader.

For now, the crown remains Nvidia's. But with Google emerging as a credible challenger and other cloud computing hyperscalers diversifing their chip sourcing, that crown sits considerably less comfortably than it did a few weeks ago.

Tesla's Pivot Eroding EV Dominance

Tesla's dominance in the electric vehicle market is eroding across all three major global markets.

European sales collapsed 48.5% in October compared to the previous year, with year-to-date sales down roughly 30% even as the broader European EV market surged 26%.

China's once-reliable market has similarly soured, with October deliveries hitting a three-year low, falling 35.8%.

In the U.S., October sales dropped 24% after a brief September surge driven by buyers rushing to capture expiring tax credits.

In Europe, Chinese automaker BYD now significantly outsells Tesla, while legacy manufacturers like Volkswagen saw sales through September reached 522,600 units—triple Tesla's European sales.

Tesla's response has been to pivot toward robotaxis and humanoid robots rather than new consumer vehicles.

CEO Elon Musk claimed Tesla will be doubling its Austin's fleet to 60 vehicles by year-end, although this is also short of his October prediction of 500.

Despite these challenges, Tesla maintains a $1.4 trillion valuation, making it the world's tenth most valuable public company by market cap.

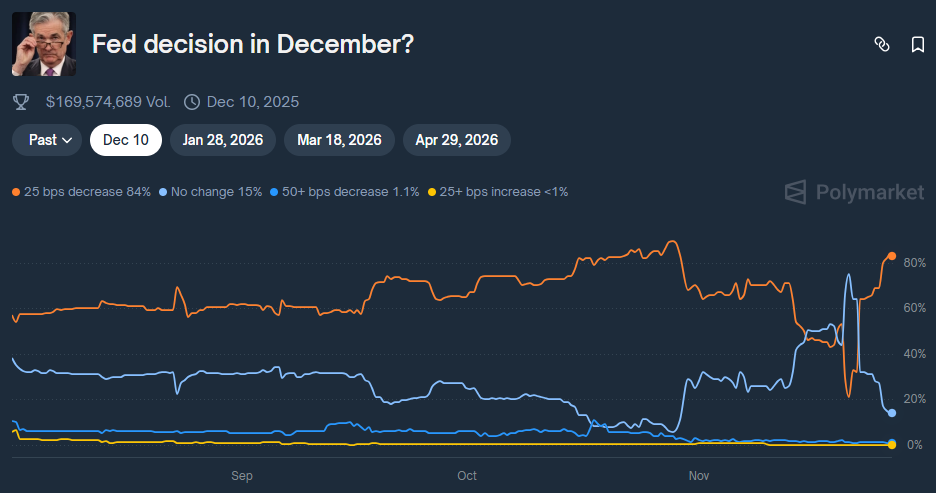

Fed December Rate Cut Flips to Certainty

Market odds for a December rate cut have flipped to above 80%, after dramatically dropping down to 42% just last week.

JPMorgan Chase has reversed its forecast entirely. After briefly predicting the Fed would delay cuts until January following delayed September jobs data, the bank now expects quarter-point reductions in both December and January.

The shift came following seemingly sudden supportive commentary from key Fed officials. New York Fed President John Williams made a case for additional rate cuts, while San Francisco Fed President Mary Daly also came out to publicly support cuts due to labour market concerns.

The sudden shift in communication means the Fed officials may have decided that market stability concerns now outweigh inflation risks — at least for now.