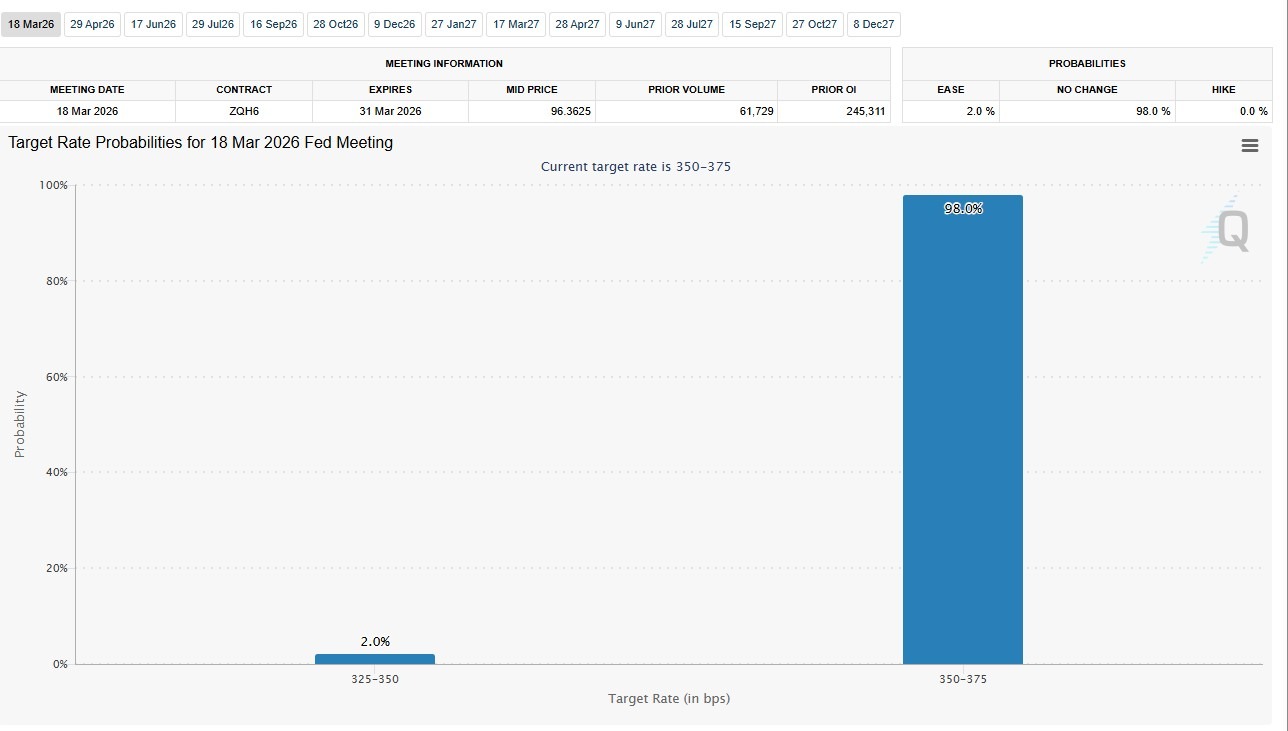

March sets up as a “repricing month” for US assets. The FOMC meeting is the centre point, with CME FedWatch showing a pause as the dominant baseline. Markets could become more sensitive to surprises in such circumstances, especially prints that alter the perceived balance between sticky inflation and slowing demand.

Rates and policy

Key dates

- FOMC meeting (two-day): 18–19 March (AEDT).

- Fed decision (FOMC statement): 5:00 am, 19 March (AEDT).

- Fed press conference: 5:30 am, 19 March (AEDT).

What markets look for

Even if rates are left unchanged, the decision can still move markets through updated projections, the policy statement, and the Chair’s guidance.

With a pause largely priced, attention shifts away from “move vs no move” and toward whether the Fed’s messaging validates the current rate path or nudges expectations toward a higher-for-longer stance or earlier easing.

Any change in the balance of risks (inflation vs growth/financial conditions) can drive a repricing in front-end rates, USD, and equity multiples.

Inflation and the link to FedWatch pricing

Key dates

- Consumer Price Index (CPI): 11:30 pm, 11 March (AEDT).

- Personal Income & Outlays/ PCE (January PCE): 11:30 pm, 13 March (AEDT).

What markets look for

When markets are anchored around a pause, inflation can become a key swing factor for the expected path of policy.

A firmer inflation profile can push the implied rate track higher and tighten financial conditions, while softer prints can reinforce the pause narrative and pull forward cut expectations.

Inflation data that arrives ahead of the policy decision tends to have greater influence on immediate repricing, while the later inflation/consumption pulse can shape end-of-month positioning and the market’s confidence in the disinflation trend.

Jobs data: the next test of rate expectations

Key dates

- ISM Manufacturing PMI: 2:00 am, 3 March (AEDT).

- ISM Services PMI: 2:00 am, 5 March (AEDT).

What markets look for

Payrolls, unemployment and wage signals can reset the tone for yields, USD and equities ahead of the major inflation and policy catalysts.

In practice, surprises often show up first in front-end rates and rate volatility, then filter into broader risk sentiment and equity pricing, especially if the data challenges assumptions about cooling demand and easing wage pressure.

Equities, tariffs and geopolitics

What markets look for

US indices remain highly sensitive to the rate narrative. The S&P 500 Index (SPX) and Nasdaq 100 Index (NDX) have traded at relatively elevated levels in recent weeks, with the VIX providing a read on implied volatility conditions.

Beyond the data calendar, the tail-end of earnings season may still generate stock-specific volatility. Tariffs and trade policy also remain a live macro risk, with official guidance for importers able to affect costs, margins and sector sentiment.

The US Supreme Court has also held that IEEPA does not authorise the imposition of tariffs under that statute. That may add uncertainty around the legal footing of Trump's tariffs.

On the geopolitical front, renewed Middle East tensions have coincided with firmer crude pricing, which may influence inflation expectations and risk appetite around CPI and Fed week (among other drivers).

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.