3月は月初に中国の経済活動およびインフレ関連データが発表され、続いて日本からも市場が注目するデータが相次ぎます。また、中旬にはオーストラリア準備銀行(RBA)の理事会が予定されており、市場では現在、政策金利の据え置きが織り込まれています。

中国

3月の中国経済は、月初から経済活動、インフレ、貿易関連の指標が集中しており、これらがアジア地域の市場心理を左右する可能性があります。市場の反応は、データそのもののサプライズ以上に、政策の解釈や流動性状況に左右される可能性があります。

主要日程

- 中国製造業・非製造業PMI: 3月2日 午後12:30(オーストラリア東部夏時間)

- 中国財新PMI: 3月5日(オーストラリア東部夏時間)

- 中国CPI(消費者物価指数): 3月9日 午後12:30(オーストラリア東部夏時間)

- 中国PPI(生産者物価指数): 3月9日 午後12:30(オーストラリア東部夏時間)

- 中国貿易収支: 3月10日(オーストラリア東部夏時間)

市場の注目点

3月の中国経済は月初にデータ発表が集中するため、最初の10日間はアジア地域の市場心理を占う上で重要な期間となるでしょう。

PMIデータは製造業やサービス業の勢いを示す先行指標となり、CPIは国内需要や価格圧力の動向を探る手がかりとなります。

上海総合指数が2010年代半ばの水準で推移する中、市場の反応は、発表される数値のサプライズ以上に、政策の解釈や流動性状況に左右される可能性があります。

日本

日本の3月は、成長の確認と、円の勢いを再調整する可能性のある政策シグナルが焦点となります。

主要日程

- 日本PMI: 3月2日 午前11時30分(オーストラリア東部夏時間)

- 日本第4四半期GDP(速報値): 3月10日 午前10時50分(オーストラリア東部夏時間)

- 日銀金融政策決定会合: 3月19日(オーストラリア東部夏時間)

市場の注目点

日経平均株価は現在史上最高値圏にあり、政策のトーンに対する感応度が高まる可能性があります。

GDPは成長の持続性と内需の動向を裏付ける材料となり、日銀のガイダンスはイールドカーブや金利見通しを左右する可能性があります。

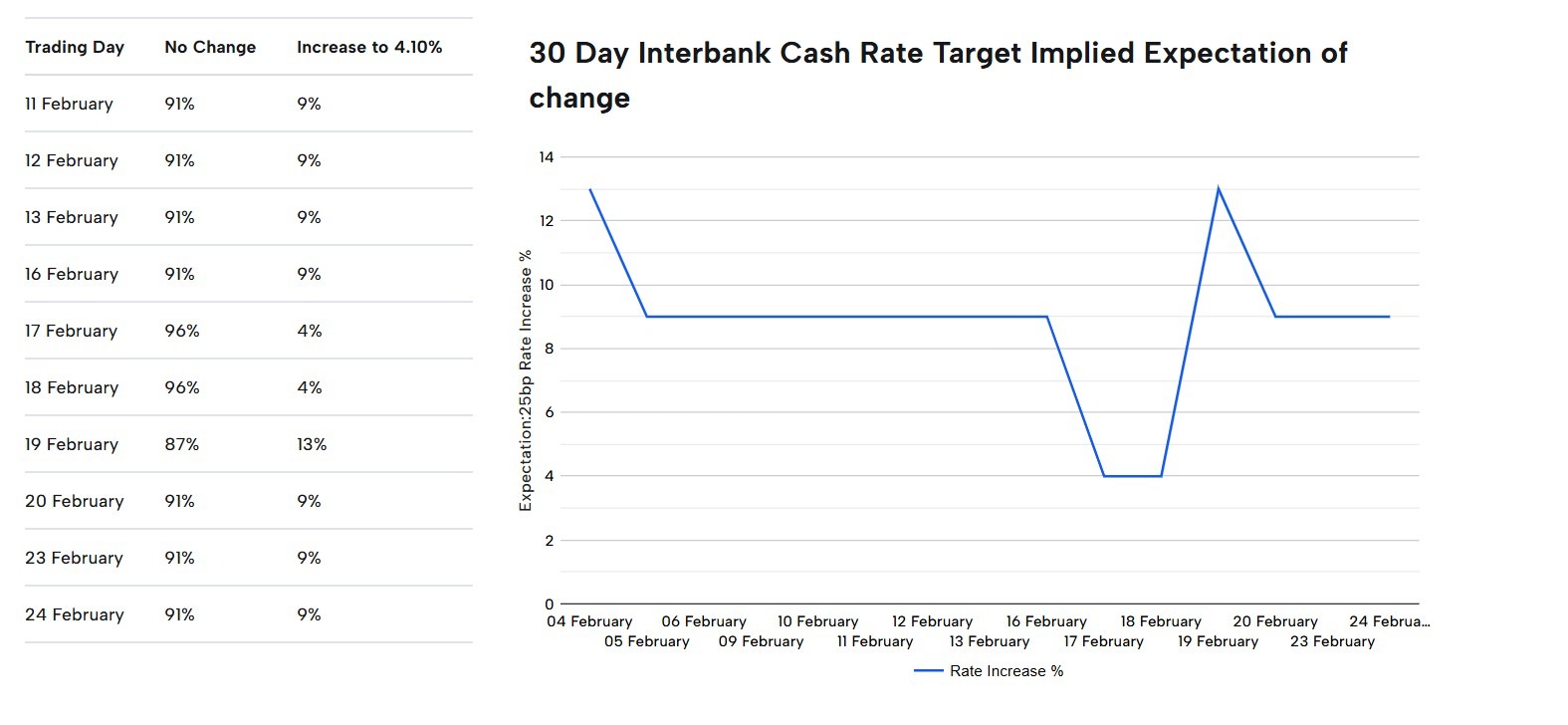

オーストラリア

オーストラリアの3月のカレンダーは、国内経済の見通しと豪ドルに影響を与え得る成長、政策、インフレのシグナルが中心となります。政策が据え置かれた場合、焦点は成長の持続性とインフレの粘着性に移るでしょう。

主要日程

- オーストラリアGDP(国民経済計算): 3月4日 午前11時30分(オーストラリア東部夏時間)

- RBA(オーストラリア準備銀行)金融政策決定: 3月17日 午後2時30分(オーストラリア東部夏時間)

- オーストラリア労働力調査: 3月19日 午前11時30分(オーストラリア東部夏時間)

- オーストラリアCPI(消費者物価指数): 3月25日 午前11時30分(オーストラリア東部夏時間)

市場の重要性

RBAの決定は金利の先行きやフォワードガイダンスを左右し、労働統計は賃金や消費の見通しに影響を与え、CPIはインフレ軌道の裏付けや修正の判断材料となります。

ASX 200は過去最高値圏で推移しており、豪ドルは主要通貨ペアに対して数年来の相対的な強さを見せています。RBAが政策金利を据え置いた場合、市場の関心は金利の方向性から、成長の持続性やインフレの根強さへとシフトする可能性があります。

Reportingdates and release times are based on company investor relations calendars whereconfirmed. Where dates or times are not marked confirmed, they are GO Marketsestimates. Consensus EPS, revenue and analyst-range data are sourced fromBloomberg and Earnings Whispers, as at 09 July 2026 (AEST). Company guidance,backlog and operating metrics are sourced from the latest company filings orresults presentations, unless stated otherwise. Any scenario analysis reflectsGO Markets analysis. Figures and schedules may change without notice.

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

Any references to Australian or international shares, sectors, indices, ETFs, crypto-related stocks or other instruments are provided for market commentary and watchlist purposes only and do not constitute a recommendation, offer or solicitation to buy, sell or hold any financial product or adopt any investment strategy. International markets may involve additional risks, including currency fluctuations, regulatory differences, market structure differences, reduced liquidity and higher volatility. Company-specific, sector-specific and macroeconomic risks may also affect performance.

Commentary on geopolitical developments, economic data, central bank decisions, earnings, policy changes and other global or financial market events is based on information available at the time of publication and may change without notice. Such events can lead to sudden market moves, price gaps, reduced liquidity, wider spreads and increased volatility, particularly in leveraged products such as CFDs. Forward-looking statements, expectations and scenario analysis are inherently uncertain and should not be relied on as guarantees of future market behaviour or outcomes.