Quick search

CLOSE+

Thank you! Your submission has been received!

이는 '비공개' 기업이 '공개' 기업으로 전환되는 지점입니다. 시장은 OpenAI, SpaceX, 그리고 새로운 ASX 상장 후보들의 내부를 처음으로 제대로 들여다보게 됩니다.

기업공개(IPO)는 비상장 기업이 처음으로 일반 대중에게 주식을 제공하는 것을 말합니다. IPO 전에는 주식이 보통 창업자, 초기 직원, 사모 투자자에게만 보유되지만, 상장하면 더 넓은 시장에서 해당 주식에 접근할 수 있게 됩니다.

트레이더에게 IPO는 한 기업의 주식에 직접 노출될 수 있는 첫 기회일 수 있습니다. IPO는 높은 변동성과 관심이 집중되는 독특한 환경을 만들 수 있지만, 가격 이력이 제한적이고 투자 심리가 빠르게 변할 수 있어 더 높은 위험도 수반합니다.

| 회사 | 추정 가치 | 거래소 | 상태 |

|---|---|---|---|

Anthropic Artificial intelligence | ~US$350 billion | Nasdaq | Rumoured |

Databricks AI and data | ~US$134 billion | Nasdaq | Expected |

Firmus Technologies AI infrastructure | ~A$6 billion | ASX | Expected |

Greencross Pet care & veterinary | ~A$4 billion plus | ASX | Rumoured |

OpenAI Artificial intelligence | ~US$850 billion | Nasdaq | Expected |

Rokt E-commerce adtech | ~US$7.9 billion | Nasdaq and ASX CDI | Expected |

SpaceX Aerospace and AI | ~US$1.5 trillion | Nasdaq | Expected |

Stripe Fintech | ~US$140 billion | NYSE/Nasdaq | Rumoured |

상장 절차는 어떻게 진행되나요

상장일이 되면 기관투자자들은 보통 이미 해당 기업을 평가한 상태입니다. 6단계 과정을 이해하면 트레이더는 주식이 더 넓은 시장에서 거래되기 전에 어떤 요인이 이미 가격에 반영되었을 수 있는지 파악할 수 있습니다.

회사는 재무 상태, 지배구조 및 시장 포지셔닝을 평가할 주관사를 선정합니다.

주관사는 실사를 수행하고 관련 규제기관에 공시 서류를 제출합니다.

경영진은 기관투자자와 애널리스트에게 회사를 설명합니다. 이 단계에서 수요가 형성되고 가격 기대치가 설정되며, 이는 개인 트레이더가 해당 주식을 보기 전입니다.

로드쇼 피드백을 바탕으로 주관사는 최종 주가를 정하고 발행할 주식 수를 결정합니다.

주식은 선택된 거래소에서 거래를 시작합니다. 대부분의 트레이더에게 이는 해당 주식을 거래할 첫 기회입니다.

상장 이후 회사는 정기적으로 재무 실적을 발표하고 해당 거래소의 지배구조 기준을 충족해야 합니다.

CFD로 IPO 거래하기

IPO 상장일은 큰 투자심리 변동과 제한적인 가격 이력으로 특징지어지는 경우가 많습니다. 이러한 조합은 전통적인 매수 후 보유 방식의 노출 관리를 더 어렵게 만들 수 있습니다. CFD는 트레이더가 가격 움직임의 양방향에 대해 견해를 취하고, 포지션 규모를 정밀하게 조절하며, 상황 전개에 빠르게 대응할 수 있게 합니다.

초기 급등 또는 열기 이후 조정을 거래하세요. CFD를 통해 상장일 이후 어느 방향으로든 포지션을 취할 수 있습니다.

IPO 변동성은 보통 첫 며칠과 몇 주에 집중되는 경향이 있습니다. CFD는 이러한 짧고 이벤트 중심적인 기간에 적합합니다.

손절매와 지정가 주문은 진입 전에 위험을 정의하는 데 도움이 될 수 있으며, 가격 발견이 아직 진행 중일 때 특히 중요합니다.

하나의 계좌로 Rokt 및 Firmus Technologies와 같은 종목을 포함한 미국 및 호주 시장의 주식 CFD에 접근하세요.

빠른 체결, 경쟁력 있는 가격, 내장형 리스크 관리 도구로 미국 및 호주 주식 CFD에 접근하세요.

So here is the thing: April’s US earnings season is arriving in a market that still feels anything but normal. As GO Markets explains in The global US earnings playbook: The essential guide for traders, this reporting period is landing after a real shift in what markets care about. It is no longer just about chasing growth at any cost. It is about what the numbers are saying beneath the surface.

And in 2026, those signals are colliding with a high-friction backdrop:

Yes, AI is still the market’s main story but it's still the flashy engine getting most of the attention. But underneath that, there is a quieter move towards companies that look built to hold up better when conditions get harder.

When rates are uncertain and energy markets are under pressure, names like JPMorgan Chase and the major defence contractors start to carry more weight. They are not replacing the AI narrative, rather, they are becoming part of the way traders read risk appetite, earnings durability and, ultimately, where the market is looking for something more solid to hold on to.

If you have been watching markets over the past year, you will have noticed that the "growth at any cost" era has effectively hit a wall. The April 2026 earnings cycle arrives at a moment when the market's focus has undergone a structural reorientation. It is not just about profit and loss statements anymore. It is about the signals sitting behind them.

With interest rate uncertainty lingering and geopolitical shocks pushing oil above US$100, the playbook has shifted from AI hype toward institutional resilience and the industrialisation of compute. For traders in Australia, Asia and Latin America, these results may act as a mood ring for global risk appetite and the emerging security supercycle.

A BMO result hits before the US cash market opens, so price discovery happens in pre-market trading where liquidity is thinner and moves can be exaggerated. An AMC result hits after close, meaning the reaction is compressed into a short pre-market window the following morning. Understanding which window your company reports in is as important as understanding what it reports.

It's worth asking: Is the obvious trade already priced for perfection?

2026 is shaping up as a year of proof. Companies that spent heavily on AI over the past two years are now being asked to show the return. The market is no longer rewarding the announcement of AI investment. It is rewarding the evidence of AI-driven revenue outcomes.

A better framing question for each result is this: are you reacting to a headline, or are you assessing the company's role in the physical AI supply chain or as a potential volatility hedge? Those are very different analytical tasks, and they tend to produce very different positioning decisions.

Here is the situation as April begins. A war is affecting one of the world's most important oil chokepoints. Brent crude is trading above US$100. And the Federal Reserve (Fed), which spent much of 2025 engineering a soft landing, is now facing an inflation threat driven less by wages, services or the domestic economy, and more by energy. It is watching an oil shock.

The Fed funds rate sits at 3.50% to 3.75%. The next Federal Open Market Committee (FOMC) meeting is on 28 and 29 April and the key question for markets is not whether the Fed will cut, it is whether the Fed can cut, or whether the energy shock may have shut that door for much of 2026.

A heavy run of major data releases lands in April. The March consumer price index (CPI), non-farm payrolls (NFP) and the advance estimate of Q1 gross domestic product (GDP) are the three that matter most. But the FOMC statement on 29 April may be the release that sets the tone for the rest of the year.

Think about what the US economy looked like coming into this year: AI-driven capital expenditure (capex) was a major part of the growth narrative, corporate investment intentions looked firm and the One, Big, Beautiful Bill Act was already in the mix. On paper, the growth story looked solid.

Then the Strait of Hormuz situation changed the calculus. Not because the US is a net energy importer, it is not, and that structural insulation matters. But what is good for US energy producers can still squeeze margins elsewhere and weigh on global demand. The 30 April advance Q1 gross domestic product (GDP) estimate is now likely to be read through two lenses: how strong was the economy before the shock, and what it may signal about the quarters ahead.

February's jobs report was, depending on how you read it, either a blip or a warning sign. Non-farm payrolls (NFP) fell by 92,000, unemployment edged up to 4.4% and the official line was that weather played a role. That may be true but here is what also happened. The labour market suddenly looked a little less convincing as the main argument for keeping rates elevated.

The 3 April employment report for March is now genuinely consequential. A bounce back to positive payroll growth would probably steady nerves and a second consecutive soft print, particularly against a backdrop of higher energy prices, would start to build a very uncomfortable narrative for the Fed. It would be looking at slower jobs growth and an inflation threat at the same time. That is not a comfortable place to be.

Here is the uncomfortable truth about where inflation sits right now. Core personal consumption expenditures (PCE), the Fed's preferred gauge, was already running at 3.1% year on year in January, before any oil shock had fed through. The Fed had not fully solved its inflation problem, rather, it had slowed it down. That is a different thing.

And now, on top of a not-quite-solved inflation problem, oil prices have moved sharply higher. Energy prices can feed into the consumer price index (CPI) relatively quickly, through petrol, transport and logistics costs that can eventually show up in the price of nearly everything. The 10 April CPI print for March is probably the most important single data release of the month, it is the one that may tell us whether the energy shock is already showing up in the numbers the Fed watches.

April is also the start of US earnings season, and this quarter's results carry an unusual amount of weight. Investors have been pouring capital into AI infrastructure on the basis that returns are coming. The question is when. With geopolitical volatility driving a rotation away from growth-oriented technology and towards energy and defence, JPMorgan Chase's 14 April earnings will be read as much for what management says about the macro environment as for the numbers themselves.

Then there is the FOMC meeting on 28 and 29 April. After the early-April run of data, including NFP, CPI and producer price index (PPI), the Fed will have more than enough information to update its language. Whether it signals that rate cuts could remain on hold through 2026, or whether it leaves the door slightly ajar, may be the most consequential communication of the quarter.

Geopolitical volatility has already pushed investors to reassess growth-heavy positioning. The estimated US$650 billion AI infrastructure buildout is also coming under heavier scrutiny on return on investment. If earnings season disappoints on that front, and if the FOMC signals a prolonged hold, the combination could test risk appetite heading into May.

Asia dominates the global semiconductor supply. Five companies, spanning Taiwan, South Korea, and Japan, sit at the critical juncture of the AI buildout, controlling everything from fabrication to the equipment that makes chips possible.

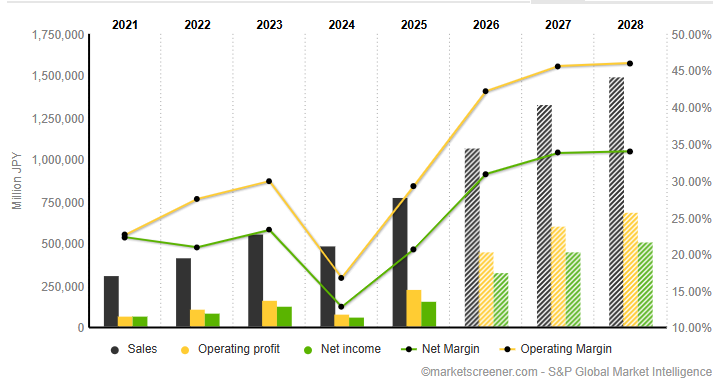

TSMC is the world's largest contract chip manufacturer, producing advanced semiconductors for Apple, Nvidia, AMD, and Qualcomm. As a pure-play foundry, it leads in 5-nanometer (5nm) and 3- nanometer (3nm) chip production, with smaller nodes in development.

The company posted $90 billion in revenue for 2024 with a 59% gross margin and 36% return on equity.

Shares delivered a total return of 55% in 2025, with analysts forecasting a further ~30% revenue increase in 2026, underpinned by its $100 billion US expansion programme.

The key risk for the company is its geopolitical exposure, with Taiwan Strait tensions remaining the sector's most-watched tail risk.

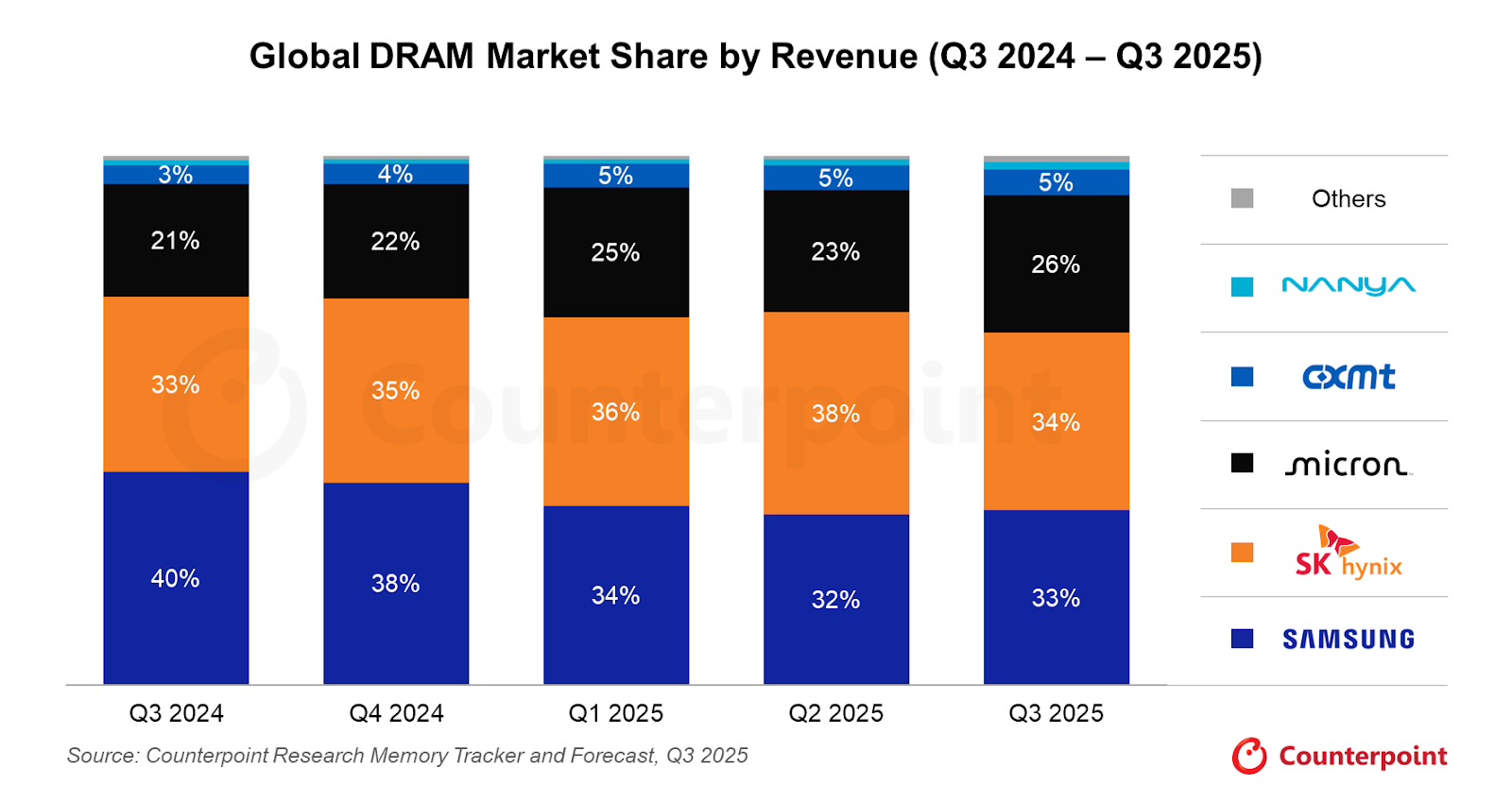

Samsung is one of the few companies globally that both designs and fabricates chips at scale. It competes across DRAM, NAND flash, and logic chip segments, and remains a core supplier to global tech giants.

Samsung's wide scope is a strength, but also a complexity. Its memory division faces margin pressure from inventory cycles, while its foundry business continues to lag TSMC in leading-edge yields.

The AI-driven memory boom may provide a tailwind, though execution in HBM production has been slower than local rival SK Hynix.

Tokyo-based Advantest makes testing equipment used to verify chips meet performance and quality standards.

It supplies to Samsung, Intel, Nvidia, Qualcomm, and Texas Instruments, allowing it to benefit from chip industry growth broadly, regardless of which foundry wins market share.

Advantest shares doubled in 2025 (+102%), and it raised its sales forecast by 21.8% and earnings forecast by 70.6% for the year ending March 2026.

Tokyo Electron is among the world's largest suppliers of semiconductor production equipment, specialising in deposition, etching, and cleaning tools.

Every major chipmaker, including TSMC, Samsung, and SK Hynix, depends on TEL's systems to scale production.

As chipmakers invest billions to expand capacity, TEL's order book grows. The risk lies in potential US export restrictions on advanced equipment sales to China, which remains one of the primary revenue segments for the company.

SK Hynix is the world's second-largest memory chip maker and has emerged as arguably the clearest AI-era beneficiary in the memory space.

It is Nvidia's primary supplier of High Bandwidth Memory (HBM) chips, the specialised memory used in AI accelerators like the H100 and B200.

HBM demand has driven a dramatic re-rating of SK Hynix's revenue profile and market standing. With AI infrastructure spending showing little sign of slowing heading into 2026, the company's HBM franchise could remain a key differentiator.

However, capacity constraints and the risk of Samsung and Micron closing the HBM gap are the primary concerns to watch.

TSMC, SK Hynix, Samsung, Advantest, and Tokyo Electron collectively control the chokepoints of the AI buildout.

The expected increase in AI infrastructure may support demand, but investors should weigh the risks carefully.

Geopolitical exposure, US export restrictions, and the pace of HBM competition could all move the needle.

So, here’s the thing...

If you have been following the tech story for the last decade, you have been trained to look at a very specific, very small patch of real estate in Northern California. But as we sit here in early 2026, the "connect-the-dots" moment for investors is this: the AI trade has stopped being about shiny software demos in Palo Alto and has started being about the physical industrialisation of compute.

Want to know more? Read our 2026 AI playbook

We have entered the "Year of Proof". The world’s largest companies, the hyperscalers, are projected to spend a staggering US$650 billion on capital expenditures this year. But here’s the part most people miss: that money is not staying in Silicon Valley. It’s flowing to the "picks and shovels" players in Idaho, Washington, Colorado and even overseas.

If you want to understand where the actual return on investment (ROI) may be landing this earnings season, you have to look outside the 650 area code. The shift from AI hype to AI industrialisation is changing the map.

Five companies · AI infrastructure play · 2026

The full AI stack: from capex to consulting

Infrastructure builders compared to the implementation bridge across the AI value chain

Hyperscaler CapEx: Early 2026 analyst estimates, midpoint of ranges. Amazon approx. 100% YoY, Alphabet approx. 100%, Meta approx. 87%, Microsoft approx. 50%.

Accenture: Cumulative advanced AI bookings $11.5B through Q1 FY2026. Q1 AI bookings $2.2B (up 76% YoY), AI revenue $1.1B (up 120% YoY) across 1,300+ clients.

Micron is the "memory backbone" of the current cycle. While everyone was watching the chip designers, many overlooked the fact that AI chips are far less useful without high-bandwidth memory (HBM). Micron is currently viewed by some analysts as a strong buy because its capacity is reportedly sold out through the end of 2026. Analysts are also eyeing a 457% jump in earnings per share (EPS) as the memory cycle reaches what some describe as a robust peak.

Microsoft is the enterprise backbone of this transition. It has moved beyond simple chatbots and is now building what analysts call "Intelligence Factories". While the stock has faced pressure recently over capacity constraints, underlying demand for Azure AI is reportedly still running ahead of capacity. The broader bull case is that Microsoft is moving into "Agentic AI", systems that do not just talk to users but may also execute multi-step business workflows.

Which Asian companies are betting big on artificial intelligence?

Amazon is playing a long-term game of vertical integration. To reduce its reliance on expensive third-party hardware, it’s building its own AI chips in-house. Amazon Web Services (AWS) remains the primary driver of profitability, and the company is using its retail data to train specialised models that many Silicon Valley start-ups may struggle to replicate.

If Micron provides the memory and Microsoft the platform, Palantir provides the "operating system" for the modern AI factory. The company has posted strong momentum, with US commercial sales recently growing 93% year over year. It’s often framed as a bridge between raw data and corporate profitability, which remains a key focus for investors in 2026.

You cannot just "plug in" AI. Businesses often need to redesign processes around it, and that’s where Accenture comes in.

The company is viewed as an implementation bridge, with one analyst arguing that "GenAI needs Accenture" to move from pilot programs to production though the cautionary angle is that the AI story has not fully excited investors here yet because consulting revenue can take longer to show up than chip sales.

The chart maps the three time horizons likely to shape the next phase of the AI industrialisation trade.

In the near term, markets are still reacting to chipmaker earnings, guidance, and any signs of capacity strain. Over the next month, attention shifts to the real-world inputs behind AI growth, especially power, financing, and infrastructure. By the 60-day window, the key question is whether AI spending is broadening into a wider market re-rating or running ahead of near-term returns.

Across all three periods, the focus is the same: proof. Investors are looking for signs that AI capital expenditure is translating into real demand for energy, land, and industrial capacity. That is why updates from companies tied to power and data centre buildout matter more than ever.

Scenario planning · March 2026

What could happen next

Three time horizons, three scenarios to watch across the AI industrialisation cycle

Chipmaker reports

Possible

Market volatility continues as traders digest the latest reports from chipmakers like Micron

Upside scenario

"Bulletproof" guidance from remaining infrastructure names triggers a sector-wide relief rally

Watch for

Any mention of "capacity constraints" or "supply bottlenecks" in earnings calls

Energy and rates

Possible

Focus shifts to "real economy" energy players like NextEra that power the data centres

Downside scenario

Rising oil prices from Middle East conflict act as a tax on tech margins, rotating into defensives

Action point

Monitor Fed language on rates. Higher for longer makes $650B capex bills far more expensive to finance

The great dispersion

Possible

Market rewards companies with real AI revenue and punishes those still stuck in experimentation

Upside scenario

NextEra Energy (NEE) data centre announcements in late April/May trigger a utility renaissance rally

Downside scenario

An "air pocket" in profits occurs where debt-funded investment outpaces revenue gains

Watch

May reports from Texas Pacific Land (TPL) — is data centre land demand still "red hot"?

Action point

Review your portfolio for geographic diversity. The AI story is now a global power race

The emotional trap many traders fall into right now is recency bias. You have seen NVIDIA and the "Magnificent 7" win for so long that it feels like they are the only way to play this. But the "obvious" trade is often the one that has already been priced in. Before acting, ask yourself: "Am I buying this stock because I understand its role in the physical AI supply chain, or because I’m afraid of missing the next leg of a rally that started two years ago?"

While all eyes are on the US AI narrative dominated by Nvidia, Microsoft, and Google, Asia has quietly been moving on AI and is home to some of the world’s most aggressive AI bets.

SoftBank is the most AI-committed company in Asia by capital deployed and ambition. CEO Masayoshi Son has declared the company in "total offence mode," having completed a $41 billion investment into OpenAI for approximately an 11% ownership stake.

Son has also launched a $100 billion initiative aimed at building a vertically integrated AI semiconductor champion (Project Izanagi), repositioning SoftBank as an "AI-era industrial holding company."

SoftBank's fortunes are now deeply tied to the success of OpenAI and Son's ability to execute his semiconductor plan that puts it in direct competition with established players.

Alibaba has committed more than US$50 billion to AI infrastructure, making it one of the largest AI capex programmes in the world.

Its Qwen family of large language models underpins a rebuilt AI-focused cloud platform, and the company has partnered with Nvidia on physical AI projects.

Alibaba Cloud is also the leading cloud provider in China. The key commercial question is whether Alibaba's can convert this cloud leadership into durable revenue growth.

However, it will have to navigate ongoing regulatory scrutiny in China and competition from local rivals like Huawei and ByteDance.

Baidu has made the most visible AI transformation of any company on this list. It has released a 2.4 trillion parameter omni-modal model (ERNIE 5.0) with approximately 70% of its search results now delivered as AI-generated rich media.

Beyond search, its Apollo Go robotaxi service is now partnering with Uber to expand into Dubai and the UK.

Its Core AI-powered business generated RMB 11.3 billion in Q4 revenue, up 48% YoY. The question now is whether that momentum is sustainable and whether the robotaxi business can scale economically.

Tencent's AI play is to allocate its GPU capacity to itself. This allows it to convert AI directly into efficiency gains across its ecosystem.

With WeChat's 1.4 billion users providing an unmatched data engine, Tencent is embedding AI across gaming, payments, cloud, and search in a way that is difficult to replicate.

This approach also offers greater resilience against AI chip export restrictions, since the compute stays internal.

The AI upside here is arguably underappreciated because it is embedded rather than a separate segment, which could also mean the market may find it harder to isolate and value that contribution.

Kakao is South Korea's dominant AI and internet platform, operating KakaoTalk, which is used by approximately 95% of South Koreans.

It is one of the most aggressively AI-focused non-Chinese tech companies in Asia, investing heavily in LLM development and AI-native services.

The domestic dominance of KakaoTalk provides a captive distribution platform for AI products in a way few companies outside China can match. The key question is whether Kakao can monetise that distribution advantage before global competitors close the gap.

Asia's AI landscape is far more complicated than a simple "follow the AI spend" narrative suggests.

China's top companies are innovating rapidly but operate under regulatory and geopolitical constraints. Japan's SoftBank is making the biggest single bet, but at a level of concentration risk that demands scrutiny. And South Korea's Kakao offers a differentiated, lower-geopolitical-risk angle.

The AI push in Asia is real. But the range of outcomes across these five names is wide, making it pivotal to understand each company's specific exposure and risk profile, not just its AI narrative.

회사, IPO 후보, 가치 평가, 거래소, 섹터 및 시장에 대한 언급은 설명 목적일 뿐이며, 게시 시점에 공개적으로 이용 가능한 정보를 기반으로 하고 사전 통지 없이 변경될 수 있습니다. 예정된 상장은 지연, 수정 또는 취소될 수 있으며, 이 페이지에 포함되었다고 해서 해당 회사가 상장되거나 특정 주식 또는 CFD가 GO Markets를 통해 거래 가능하다는 의미는 아닙니다.