- Trading

- Trading

- Markets

- Markets

- Accounts

- Accounts

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Premium trading tools

- Premium trading tools

- Education

- Education

- Resources

- Resources

- Help & support

- Help & support

- About

- About

- Client support

- Trading

- Trading

- Markets

- Markets

- Accounts

- Accounts

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Premium trading tools

- Premium trading tools

- Education

- Education

- Resources

- Resources

- Help & support

- Help & support

- About

- About

- Client support

News & analysis

News & analysisFX – The Uncertain Peak: Assessing the Current State of Inflation and Interest Rates

30 April 2024As April draws to a close, the global economy stands at a pivotal juncture, grappling with the resurgence of inflationary pressures that refuse to retreat. In fact, it feels as though the inflation genie has re-emerged, asking, “Oh, you want more?”

This resurgence prompts a crucial question: have we truly witnessed the peak of inflation, and consequently, the peak in interest rates, or are we merely witnessing a temporary lull before central banks are compelled to escalate interest rates further?

The market has become entangled in this debate over the past few weeks, and it’s far from reaching a resolution.

At the heart of the matter lies ‘sticky’ inflation. Economies such as Australia, the United States, and New Zealand are grappling with persistent price increases in essential fixed goods and services, including insurance, rent, housing costs, and utilities. The resilience of inflation in these sectors underscores the enduring impact of global economic forces on household budgets.

Remarkably, despite facing a post-COVID landscape fraught with challenges, households in these nations have displayed remarkable resilience. They have weathered the storm of rising interest rates while managing to maintain or marginally adjust their spending habits. Such resilience would typically be viewed as a positive narrative in a conventional economic cycle, signaling prudent financial management and adaptability.

However, the current economic landscape is anything but conventional. Against the backdrop of a global interest rate cycle reaching decade-high levels, the resilience of households and the absence of significant spending contractions raise concerns. Will tentative central banks be forced to raise rates again, rather than enact the forecasted rate cuts that were almost certain just eight weeks ago?

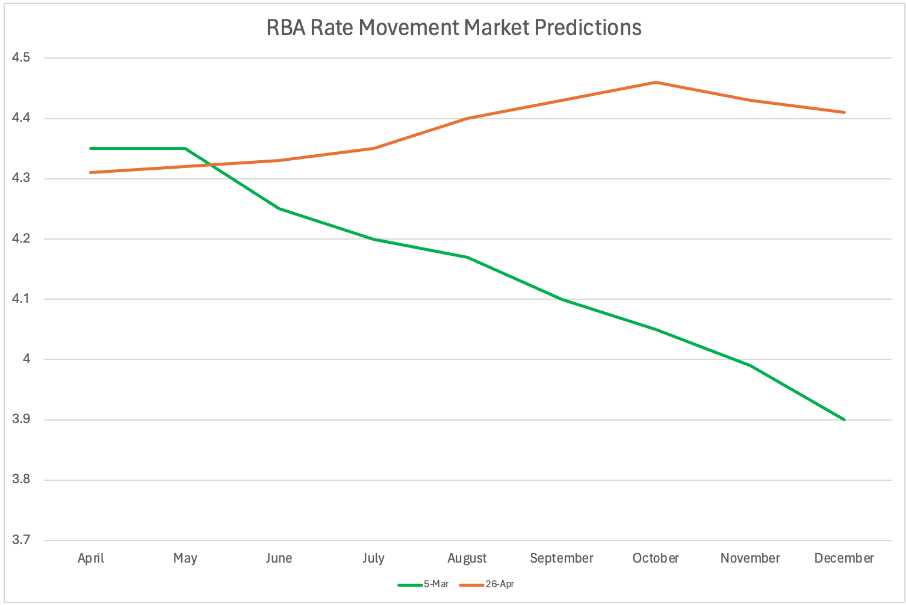

The chart depicting the change in the 30-day interbank cash rate implied yield curve from the start of March to the end of April vividly illustrates this shift. The difference is staggering.

The resurgence of inflationary pressures threatens to upend optimistic projections. It challenges the notion that the peak of the current economic cycle has already been reached. Instead, it suggests that the trajectory of interest rates may continue to trend upward, defying earlier forecasts and unsettling financial markets.

From and FX perspective this is creating and interesting situation in the policy divergences of other central banks.

The US is facing a similar issue to that of the RBA – market pricing for the Federal Funds rate has gone from a fully pricing in 3 rate cuts with the real possibility of a 4th in 2024 too just 1 rate cut in 2024 and only 2 cuts in 2025. Both are facing much higher rate situations in 2024.

Compare that to the likes of European Central Bank (ECB), Swiss National Bank (SNB), Bank of Canada (BoC), and the Riksbank. All are signalling potential rate cuts in upcoming meetings. In the case of the ECB it looks like being as early as June.

This policy divergence creates significant implications for FX markets. Bullish bets in the AUD have been coming thick and fast as interest rate differentials has seen crosses moving firmly in the AUD’s favour. EURAUD, AUDCAD, AUDJPY and the likes

In the case of the AUDUSD this pair is hard to read as both have similar dynamics. The rule of thumb in a scenario like this is ‘all roads lead to the USD’ and explains why the AUD is lagging in this pair but not elsewhere.

On the USD – the clearest example of the pressure it is putting on the rest of its peers is USDJPY.

For the first time since 1990 USDJPY passed Y160. It would appear this is a market test for the Bank of Japan. Does it defend its falling currency? Does it lose its authority due to it losing control of its control mechanism? The economic fundamentals make this a very interesting question indeed.

Ready to start trading?

The information provided is of general nature only and does not take into account your personal objectives, financial situations or needs. Before acting on any information provided, you should consider whether the information is suitable for you and your personal circumstances and if necessary, seek appropriate professional advice. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice. Past performance is not an indication of future performance. Go Markets Pty Ltd, ABN 85 081 864 039, AFSL 254963 is a CFD issuer, and trading carries significant risks and is not suitable for everyone. You do not own or have any interest in the rights to the underlying assets. You should consider the appropriateness by reviewing our TMD, FSG, PDS and other CFD legal documents to ensure you understand the risks before you invest in CFDs. These documents are available here.

#Forex #ForexAnalysis #ForexBroker #ForexCharts #ForexMarket #ForexNews #ForexSignal #ForexTradingNext Article

Inside the Fed

Let us open with this: “It’s unlikely that the next policy rate move will be a hike. I’d say it’s unlikely,” – US Chair Jay Powell This verbatim quote puts a lid on the movements seen in bond and interbank markets that might have overacted to recent data that has been above expectations and has led some to price hikes. The let u...

May 2, 2024Read More >Previous Article

FX Analysis – EUR Rate divergence rhetoric fading?

With an ECB June cut looking likely, FX traders will start looking at the policy path beyond June. Most analysists are calling that the European Centr...

April 26, 2024Read More >

- Trading

- Trading

- Trading

- Markets

- Markets

- Products overview

- Forex

- Commodities

- Metals

- Indices

- Shares

- Cryptocurrencies

- Treasuries

- ETFs

- Accounts

- Accounts

- Compare our accounts

- Our spreads

- Funding & withdrawals

- Open CFD account

- Try free demo

- Platforms & tools

- Platforms & tools

- Platforms

- Platforms

- Platforms overview

- GO Markets trading app

- MetaTrader 4

- MetaTrader 5

- cTrader

- cTrader copy trading

- Mobile trading platforms

- GO WebTrader

- Premium trading tools

- Premium trading tools

- Tools overview

- VPS

- Genesis

- Education

- Education

- Resources

- Resources

- News & analysis

- Education hub

- Economic calendar

- Earnings announcements

- Help & support

- Help & support

- About

- About

- About GO Markets

- Our awards

- Sponsorships

- Client support